Signature Delegation Introduction

This information is intended to outline the origins of signature delegation policies and procedures, definitions, roles and responsibilities and resources related to Programmatic Approval delegations, Fiscal Approval delegations and Budget Approval delegations. This information will discuss the parties involved in delegated approvals, transaction types requiring review and approval, how delegations are managed, frequency of delegation review, and when dual approvals are appropriate. Most audits or compliance reviews contain a review of authority to approve transactions. Documented delegations are key to this process.

Programmatic Delegation

The chief administrative officers in each area have the responsibility to develop, operate, and maintain an organization that achieves maximum performance with the available resources at their disposal. They are expected to exercise prudent judgment in the expenditure of funds and the utilization of services. They are responsible for ensuring that all programs and actions conform to the appropriate University policies.

As the chief administrative officers, Directors, Department Heads, Deans, Vice Presidents, and Vice Provosts should be familiar with University fiscal rules, regulations and policies, and should take steps necessary to ensure that they are followed. In many areas, Business Office staff are responsible for assisting administrative officers in fulfilling their fiscal responsibilities of budgeting, payroll, staff benefits, personnel, purchasing, accounting and sponsored programs administration. However, Business Office staff are not authorized to make academic decisions or to commit funds other than those agreed to by the chief administrative officer, who has final responsibility for all fiscal aspects of their operations.

Transactions, inclusive of Effort Certification, require programmatic approval to charge to sponsored program accounts. Principal Investigator (PI) expectations are outlined in the Expectations of a Principal Investigator resource. These expectations indicate that PIs provide oversight of sponsored funding including timely notification to the Business Office of delegating signature authority to staff within their lab.

Business Offices are responsible for maintaining a record of authorized delegates for each PI and to review transactions per the established guidelines, checking for appropriate programmatic approval.

WHO SHOULD BE DELEGATED AUTHORITY?

HOW SHOULD DELEGATIONS BE DOCUMENTED?

Each year, Purdue University is subject to an annual single audit which is performed by an independent external accountant. This audit is a fundamental part of the process of publishing the annual financial report of the University and assessing compliance with federal regulations in accordance with Uniform Guidance regulations established by the Office of Management and Budget. As part of the audits, key university administrators are required to sign a certification statement regarding the completeness of financial data and effectiveness of the internal control structure. This is done through the Annual Financial and Compliance Certification.

The colleges and schools of the West Lafayette campus, the regional campuses, and the various other administrative units play a critical role in the financial integrity of the University. Chancellors, deans, vice presidents, vice chancellors, department and unit heads make strategic, operating, and business decisions regularly. Business officers within these unit’s exercise delegations of authority from the Treasurer and Chief Financial Officer to carry out these decisions in accordance with the University policies and state and federal laws and regulations. The financial integrity of the University is embedded in the activities conducted in the operating units of the institution.

Significant aspects of financial reporting and internal controls are implemented, managed, and monitored at the college, school, division and departmental level. Due to this structure, the Annual Financial and Compliance Certification Form was developed to support the assurances made to the University’s external auditors.

Each year, the administrative leader and financial officer reviews the certification form, which includes the following statements:

- Staff responsible for operating accounts have been made aware of and understand the policies, procedures, and regulations for the use of such accounts including general funds, grant funds, contract funds, and gift funds. Oversight is provided to ensure the grant, contract, and gift funds are used for the purpose for which they were intended.

Signature authorizations for the area of responsibility have been reviewed to assure they are valid and appropriate. Individuals with signature authority have been made aware of their responsibilities and accountability for transactions.

In addition to the annual Financial and Compliance Certification process and form, delegation of authority for procuring goods and services on sponsored programs requires a signature authorization record be maintained in the Business Office with the Principal Investigator approval for their designees. The PI must communicate in a timely manner the names, accounts, and purchasing limit per delegate to the PI’s Business

Most programmatic approvals are collected outside of electronic workflow and should be kept with other backup documentation and available upon request.

Another type of programmatic delegation is called a Certification. Generally, certifications are done by PI’s or other programmatic staff to certify allocability or benefit to a project. Examples of certifications are the approval of a PAR via SEEMLESS or the certification of benefit to a project on a correcting document. The Effort Reporting Policy and Procedures address who can certify a PAR and to whom the PAR certification process can be delegated.

HOW FREQUENTLY SHOULD DELEGATIONS BE REVIEWED?

Directors of Financial Affairs (DFA) or Assistant Directors of Financial Affairs (ADFA) should review programmatic delegations with Unit Leaders on at least an annual basis. The table below lists documents that require programmatic (academic) approval and cannot be delegated (column 1), and those that can be delegated and approved by an authorized (fiscal) delegate (column 2):

| Documents Requiring a Chief Administrative Officer Programmatic Approval | Documents that Can Be Approved by Authorized Fiscal Approver Delegates |

| Proposals/COEUS Proposal Submissions | Ariba Orders |

| Request for Notice to Proceed (Form 27) | Direct Invoice Vouchers (ZV60) and Credit Memos |

| All Leave related documents (automatic workflow in SuccessFactors) | PRF Discretionary Request Form |

| Employment Contracts (Form 19, 19E, 19L) | PRF Deposit Form |

| Overload authorization | Electronic Work Orders (Physical Facilities), with proper role |

| Personnel Activity Reports (PAR)* | Transportation Form 1 |

| Outside Activity Form | Journal Vouchers (FV50) |

| Cost Sharing (Form 32) | Employee Data Changes/Actions in SuccessFactors |

| Conflict of Interest Disclosure | Additional Pay Request Form (ADPAY) |

| Voluntary Support/Gift Report (Form 44) | Graduate Fellowship Assignment (eForm 90) |

| Gift in Kind (Form 41B) | Property Off Campus Forms |

| Flight Operations request | |

| Payee Certification Form* |

*Requires certification of benefit to grant or federally appropriated fund.

PI delegations of purchasing authority for account specific authorization should be reviewed on a regular basis to keep the delegations records current.

WHAT SHOULD BE REVIEWED?

All disbursement transaction types inclusive of Ariba, Direct Invoice Voucher, Purchase/Travel Card, Travel Expense Reports, iLab and non-iLab Recharge Center postings, and Payroll and Effort Certification require programmatic approval.

The following items should be reviewed to ensure programmatic approvals are valid.

- The expense is consistent with department goals, objectives, and needs.

- The expense has been authorized by someone with first-hand knowledge of the need for the item and that person has the authority to commit funds.

- The source of funds is appropriate for the transaction.

- Split allocation should have the % allocation to each account noted and provided the allocation method used for unusual split percentages.

Fiscal Approval Delegation

In addition to assisting chief administrative officers in meeting their responsibilities, Business Office staff have also been delegated specific signature authority on procurement and disbursement documents. This signature authority is derived from the Bylaws of the Board of Trustees and through delegation from the Executive Vice President and Treasurer. The Bylaws of the Board of Trustees state that, “no disbursements shall be made, or moneys collected, used or distributed in conduct of the Corporation of the University and their business without authorization of the Treasurer.” This delegation is approved by the Comptroller.

Current policies governing fiscal delegations are:

- EVPT Memo A-19 (March 7, 2000) – under review

- Delegation of Authority and Responsibility for Making and Executing University Contracts and Written Agreements (Except Employment Contracts)

- EVPT Memo A-35 (March 7, 2000) – under review

Delegation of Signature Authority for Approving the Obligation of University Funds for Procurements of Services, Supplies and Expenses, and Capital

WHO SHOULD BE DELEGATED AUTHORITY?

MANAGING FISCAL APPROVAL AUTHORITY AND EXPECTATION

HOW IS FISCAL APPROVAL DELEGATION MANAGED?

Fiscal approval delegation is managed through an SAP role on the position. Delegated individuals should have the SAP role and appropriate Business Area and Fund Center assignments through the Fiscal Approval Table in SAP.

Please note in the fiscal approval tables below that with the implementation of the 2018 Transformation Project, transactions less than $1,000 do not require prior fiscal approval. A best practice review titled Monthly Review of Transactions Without Prior Fiscal Approval – <=$1,000 on federal funds was implemented in August 2021. See the Sponsored Program Services Post Award Account Management website for documents including best practice, QRG for running report, FAQ’s for the process, a training presentation as well as a link to the actual training related to this best practice.

For information on assigning the role to a position in SAP, see: Business Process – Roles and Privileges.

Workflow on certain transactions is automatically derived when routed through fiscal approval workflow based upon the role & table.

Requests for changes to the fiscal approver table can be made at Fiscal Approver Changes.

FISCAL APPROVAL LEVELS BY POSITION

| Level | $ Limit | Position Delegated Authority |

| 0 | $1,000 or less | Fiscal Approval Not Required |

| 1 | $1,001-$5,000 | Account Assistant or higher |

| 2 | $5,001-$25,000 | Business Manager or higher |

| 3 | $25,001-$100,000 | DFA, ADFA, Business Manager or higher |

| 3 | Pre-Auditor | Designated Pre-Auditor |

| 4 | $100,001-$500,000 | Senior DFA or Vice Chancellor Fiscal Affairs |

| 5 | $500,001-$1,000,000 | Deputy CFO, AVP Finance |

| 6 | $1,000,001-$2,000,000 | Treasurer, Deputy CFO, AVP Finance, Director of Central Finance (PWL) for Capital Project Exp over $100k (Financial Units 990×06) and PWL Central Office (BA4000) |

| 7 | $2,000,001 or higher | BOT through the Treasurer |

FISCAL APPROVER ROLE BY POSITION

| Level | $ Limit | SAP Role | Typical Position with Role |

| 1 | $1,001 – $5,000 | External_SRM_SM240_000 – Level 1 | Account Clerk/Assistant or higher |

| 2 | $5,001 – $25,000 | External_SRM_SM245_000 – Level 2 | Business Manager or higher |

| 3 | $25,001- $100,000 | External_SRM_SM250_000 – Level 3 | ADFA/DFA or higher Large School Business Managers may also have level 3 authority. |

| 4 | $100,001 – $500,000 | External_SRM_SM255_000 – Level 4 | Senior DFA or Vice Chancellor Fiscal Affairs |

| 5 | $500,001- $1,000,000 | External_SRM_SM250_000 – Level 5 | Deputy CFO, AVP Finance |

| 6 | $1,000,001- $2,000,000 | External_SRM_SM500_000 – Level 6 | Treasurer, Deputy CFO, AVP Finance, Director of Central Finance (PWL) for Capital Project Exp over $100k (Financial Units 990×06) and PWL Central Office (BA4000) |

| 7 | $2,000,001 or higher | N/A | BOT, but it routes to the Treasurer and then the Treasurer takes it to the Board. |

Important information regarding updates to the fiscal approver table:

- You can review the current approvers in the approver table with t-code ZFI_WF_APPROVERS in SAP S/4

- Approvers are assigned by position number, not the Personnel Number (PERNER) or Person ID

- Only one person can be marked as Primary approver at Level 1 or Level 2 per cost center for Concur. Concur Reconcilers cannot be a Concur approvers

- Business Area Fiscal Approvers are only set at Level 3 (SPS pre-audit) or Level 4. When requesting Pre-audit, balance sheet, or federal appropriations fiscal approvers these are entered for the business area and should not contain an indication of cost center. For more information, please go to Pre Audit.

HOW IS FISCAL APPROVAL DELEGATED?

Employees in positions eligible for fiscal authority earn fiscal approval authority after a period of learning and practice. The process varies by unit, but the learning period can last 6-12 months, and includes:

- Successful completion of available trainings. Work with your supervisor to identify needed trainings.

- Regular review of documents and workflows with an experienced fiscal approver.

- Readiness assessment performed by someone who has fiscal authority. The assessment questionnaire should be used within this handbook.

WHAT SHOULD BE REVIEWED?

Many questions must be answered before final approval can be granted for procuring goods and services on University-controlled funds. The purpose of this document is to provide fiscal guidelines for staff who are involved in the fiscal approval process. These guidelines are intended to provide a general framework for the approval of transactions. An understanding of circumstances unique to a school, department or office will also aid an individual in the approval process.

Sponsored Program expenditures should be authorized by someone with first-hand knowledge that the requested expenditure benefits the designated project. It is inappropriate for Principal Investigators to delegate their authority to the business office as business officers do not have first-hand knowledge of project benefit.

The Principal Investigator may delegate his or her authority to designated lab managers, which is typically documented on the PI Grant Signature Delegation Form.

Business office staff with fiscal approval delegation should ensure the tests for allowability, allocability and reasonableness have been met. Business office staff may aid in the determination of allowable costs, provide guidance in the determination of appropriate cost allocation techniques, and ensure certifications are obtained on source documents and that these documents are retained in accordance with University retention requirements.

ALLOWABILITY, ALLOCABILITY, AND REASONABLENESS

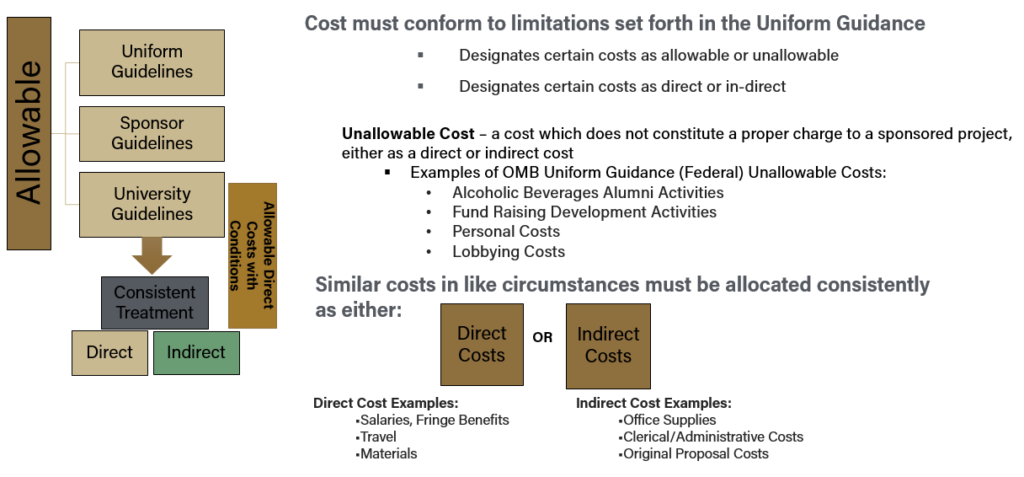

Allowability: Cost must conform to limitations or exclusions as set forth in Uniform Guidance, which designates certain costs as allowable or unallowable and designates certain costs as direct or indirect.

- The transaction must meet the restrictions imposed by donor, external provider and the University. Fund accounting allows the University to segregate funds by source. Funds with similar characteristics (e.g., common source or similar restrictions) are grouped together. For a transaction to be allowed, it must comply with funding restrictions placed on the use of the funds by the provider (source) and support the University’s mission. Restrictions placed on general funds of the University relate to three primary sources of revenue: student fees, state appropriations, and facilities and administrative cost recovery. Additional scrutiny should be applied to a transaction if you as a student, taxpayer or auditor would question the legitimacy of the transaction for the identified activity.

Examples of these items are: Purchasing flowers from general funds as props for a play produced by the University Theater Department as part of the education of theater students supports the mission. Purchasing flowers for the Payroll Office does not.

- For federal funds, the transaction must meet the restrictions imposed by the federal government, OMB Uniform Guidance – 2 CFR 200. In addition, all other funding sources have restrictions placed on uses by either the University donor, bond indenture or other external

Figure 1: Allowability Review

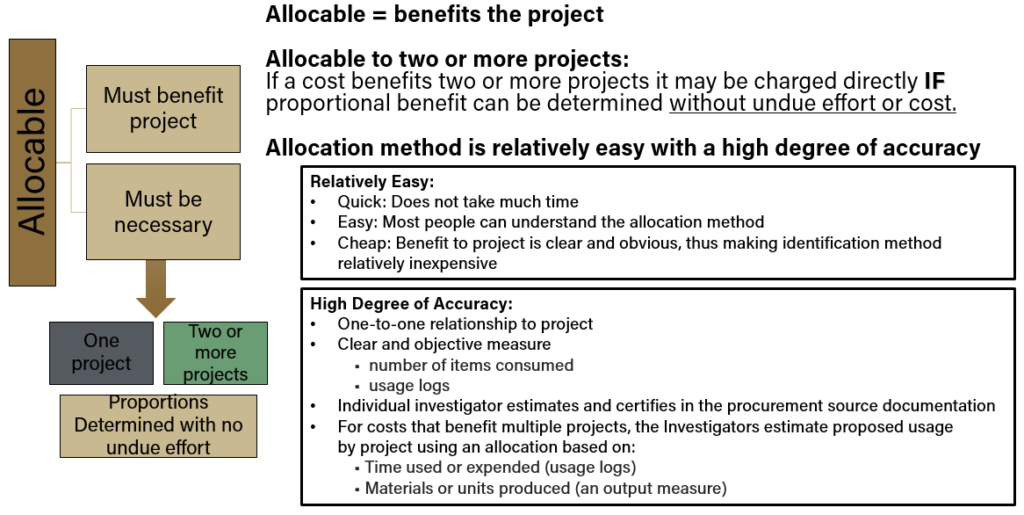

Allocability: The expenditure provides a direct benefit to the project (i.e., the cost of a piece of equipment that is required to accomplish the work and meet the objective of the project’s statement of work).

- Is there evidence that someone with firsthand knowledge determined that the purchase benefited a particular project?

- The transaction is allocable if the individual requesting the item certifies that:

- He/she has authority to commit funds on the proposed funding

- He/she certifies that the transaction will benefit, or equitably benefit, the identified funding source(s).

- He/she certifies that funds are available for the

When allocating costs to multiple projects, there must be documented proportional benefits to each of the projects. A cost that benefits two or more projects in proportions that can be determined without undue effort should be allocated to the projects based on the proportional benefit. The allocation must take into consideration the benefit of the cost within the time remaining on the project.

Examples of these items are: A PI wants to purchase a number of chemicals on three separate projects. The total cost of chemicals was $850.00 for 16 pounds.

| Project | $’s | % | Method |

| 1 | $425.00 | 50% | Used 8 pounds |

| 2 | $212.50 | 25% | Used 4 pounds |

| 3 | $212.50 | 25% | Used 4 pounds |

Figure 2: Allocability Review

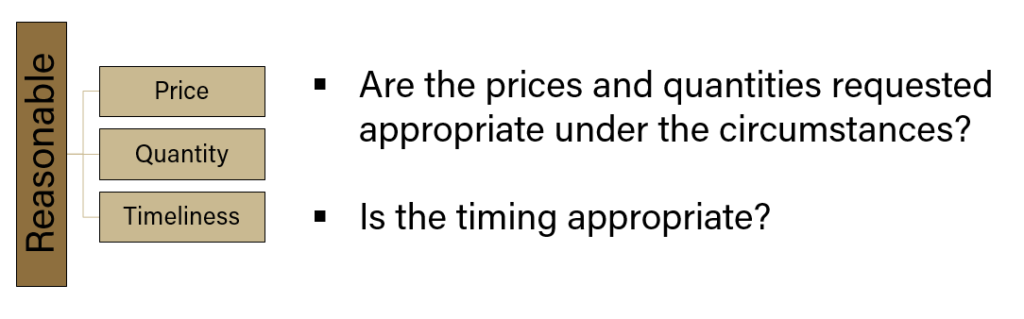

Reasonableness: The nature and amount of the expenditure reflects an action that a prudent person would take under the circumstances.

- The procurement would be considered reasonable if BOTH quantity and price of the proposed item would be considered appropriate by a prudent person given circumstances prevailing at the time the decision to procure goods and services was made. The item must also be necessary to conduct the work of the office or department incurring the cost.

- Is purchase considered appropriate based on length of time left in the project period?

Figure 3: Reasonableness Review

FISCAL APPROVAL REVIEW LIST

To aid with understanding what needs to be reviewed for different types of documents, the Fiscal Approver Document Review Grid

PRE-AUDIT

A) PRE-AUDITOR DELEGATION:

The Associate Vice President of Sponsored Program Services grants SPS Pre-Auditor Delegation. Documents that receive Pre-Audit approval include correcting documents (Journal Vouchers (tcode FV50 Document Type SA), Late Personnel Activity Reports (PARS) and Revised PARs (via SEEMLESS), CD-01 Payroll Distribution Changes for True Fellowship staff and iLab Corrections on Sponsored Program or Federal Appropriations.

See Pre-Audit for Pre-Audit Process and Lifecycle of an Account – Policy Training Program for Pre-Audit training recording and presentation.

B) PRE-AUDITOR EXPECTATIONS:

· PRE-AUDITORS ASSURE COMPLIANCE WITH:

- University rules, regulations and policies

- Federal cost allocation guidelines

- Sponsor Guidelines

· PRE-AUDITOR EXPECTATIONS:

- Knowledge of University, Sponsor and Donor policies and procedures

- Knowledge of Sponsored Program Administration

- Demonstrated Excellence in: preparing and reviewing documents, reviewing support documentation, following proper retention policies, and communicating unique situations or circumstances

· ROLE OF PRE-AUDITOR:

- Assure compliance with the document preparation guidelines

- Assure sufficient explanation

- Verify appropriate certifications have been obtained

- Assure change is allowable, allocable, reasonable, and timely

- Assure that movement is needed and is not done solely for convenience or funds availability

- Communicate revisions or corrections to the document preparer and initiate appropriate corrective actions

- Provide feedback about why changes are needed

- If not electronically routed, forward document to proper office

- Journal Vouchers route electronically

- Late and Revised PARs must be selected in SEEMLESS

- Paper PARs are outside of SEEMLESS

- CD-01 for True Fellows are on paper

- iLab corrections are pre-audited and approved outside the iLab system but entered via iLab with exception to corrections that move charges using Voluntary Cost Share G/L, for which the correction is completed via FV50 SA document.

- If transaction could be questionable, add explanation of rationale when appropriate

Dual Role – Delegated Signature Authority

Budget Approver Delegations

SuccessFactors is an SAP product used at Purdue University to manage HR related data and transactions and has its own roles and privileges. See the SuccessFactors Roles and Privileges site for SuccessFactors related details and SAP Identify Management (IDM) – Roles and Privileges for details on request roles.

Recruiting

WHO HAS THE ROLE

Certain business office staff are responsible for budget approvals in SuccessFactors during the recruitment stage. The initiator of the requisition is responsible for adding in the appropriate Budget Approver into the requisition based upon individual unit expectations. Generally, this is the Business Manager, ADFA or DFA. All requisitions require approval by the Budget Approver in order to proceed with hiring with the exception of students and post-doctoral researchers/LTL/temporary staff. The Budget Approver will review the requisition details including verifying and adding the budgeted salary information.

The Budget Approver is responsible for approving offer letters for staff and faculty hiring. For staff hiring, the HR Talent Acquisitions teams will add the appropriate Budget Approver from the requisition to approve the offer details such as offering hourly rate or salary. The Budget Approver should ensure the offering salary and FTE align with the budget for their unit. For faculty offers, the Faculty Offer Letter, Approval Process and Post Offer Tasks should be followed. Note that some colleges have additional internal approvals as part of their offer letter process. Your Unit Lead or DFA are familiar with those additional requirements.

HOW IS THE ROLE ASSIGNED?

During the recruitment stage, the Budget Approver is manually added to the requisition and offer letter approval. Once added into the workflow, the approvals will appear in the To Do Tile in SuccessFactors.

WHAT SHOULD BE REVIEWED?

- Have appropriate approvals been obtained to fill the position?

- Is there sufficient funding to support the position?

- Is the funding source appropriate and/or position budgeted?

- Is the funding end date (if applicable) appropriate to support the proposed duration of the position?

- Is the targeted salary or hourly rate within the budget?

Employee Action/Data Change

WHO HAS THE ROLE?

Certain business office staff have been assigned the Budget Approver role in SuccessFactors for approving employee data changes, payroll actions and terminations. The role is generally assigned to the Business Manager level and above.

These actions requiring approval include change in pay, AY/FY conversions, transfers, FTE changes, employment type changes, and terminations.

HOW IS THE ROLE ASSIGNED?

The role is managed in the SAP Identify Management (IDM) system, used to track business roles approved for specific positions. The Budget Approver role for data changes is assigned to a position and provisions access to the employee who holds the position. As an employee transitions into or out of a position, roles get automatically provisioned or removed based upon the roles of the position.

The Business Role name assigned to this group is Business Manager Role and encompasses many privileges for SuccessFactors and ECP.

HOW DOES WORKFLOW WORK?

The Budget Approver is automatically added into the electronic workflow in SuccessFactors for predetermined actions requiring fiscal review.

Actions will appear in the Approve Requests tile in the To-Do section of the SuccessFactors homepage.

WHAT IS REVIEWED?

Budget Approvers should reference the Employee Data Change training resources for specific reference guides based upon the employee action or data change.

Additional Resources

Appendix A – Fiscal Approval Assessment Questionnaire

Purchasing Documentation Review

This document should be used when reviewing purchasing documents with the staff member being assessed for fiscal approval delegation. This should be used to assess a person’s readiness to assume the responsibility for a fiscal approver. Questions in the second category build on the first category. For instance, a $5,235 purchase would need to have the questions in both the <$5000 category and the <$25,000 category addressed.

<$5,000 PURCHASE LEVEL REVIEW

- How was the need for the purchase communicated? Is there sufficient back-up documentation?

- Is the document filled out completely and correctly?

- Is this a valid WBSE or IO for this transaction?

- Does the requester have authorization for the account number being used? If not, has authorization been documented?

- Are there sufficient funds in the account? How did you verify this?

- How did you decide on the GL to use? If you were unsure, whom did you ask for clarification?

- Was the correct purchasing process used? How did you arrive at this conclusion?

- If the account is a SPS account, was the purchase allowable? If you weren’t sure, whom did you ask for clarification?

- Is the purchase appropriate for the WBSE or IO? If you were not sure, how did you find out it was okay to use the fund/cost center for this purpose?

- Who should approve the document? On what did you base your decision?

- On sponsored research funds for capital purchases, does the sponsor require specific approval? If so, was the item noted in the approved budget? How did you find out? If not, what did you do? Why? (Prior approval process? Switch accounts?)

- Was an equipment screening process required? If unsure, how did you find out?

- Is the purchase reasonable? How did you arrive at your conclusion?

- If a sponsored program account, was the purchase initiated in a timely manner when considering sponsor and project period requirements?

<$25,000 PURCHASE LEVEL REVIEW

Assuming the person has demonstrated mastery of the concepts required for the <$25,000 level of signature delegation:

- Was the transaction completed in the most efficient manner?

- Does the transaction correspond to the goals and mission of the School/University?

- In accordance with OMB Uniform Guidance, 2 CFR 200, was the appropriate equipment screening process followed?

Appendix B – Fiscal Approval Document Review Grid