Accounting and Financial Management Governance – Finance Topics

AG AND STATELINE

AG AND STATELINE FUNDS

AG FUNDS

- Funds that are unique to the College of Agriculture.

- Identify sources of income that have originated from the State or Federal legislatures.

- Because Purdue is a Land-Grant Institution, it has been designated as the recipient of funds allocated to fulfill the goals of the State and Federal governments.

- These funds are categorized into three missions:

- Instruction (Learning)

- Extension (Engagement)

- Research (Discovery)

AG FUND TYPES

GENERAL FUNDS

- General Funds are separated by mission for matching and reporting requirements.

- 21010000 – Instruction

- 21020000 – Extension

- 21030000 – Research

- Fund 21040000, previously used specifically for International Programs, has been removed and those funds will now be included in the 21010000 funds

- Expenses should be charged according to mission of the fund.

- General purpose items or support staff should be split according to effort.

- Example: A copy machine for a main office can be split equally between 2101, 2102, and 2103.

- Lobbying Costs should be tracked separately or by using the GL Commitment Item 546440 (Restricted Costs).

- This GL Commitment Item is not used in the F&A Cost Study.

- Hospitality and Entertainment Costs are recorded using the GL Commitment Item 546435 in accordance with University policy.

- These are not allowed on Federal Formula Funds.

- Use of this GL Commitment Item allows for proper treatment for &A Cost Study.

STATE LINE APPROPRIATIONS

- State Line Appropriations are separate from General Funds and are used to support a specific Ag priority area.

- 32020000 – Extension Educators

- 32030000 – State Extension (Crossroads and Ag SEED)

- 33080000 – State Research (Crossroads and Ag SEED)

- General Fund guidelines apply according to the mission of fund.

- Fund 32020000 is only used by County Extension Services (CES) for Extension Educator salaries.

REGULATORY FUNDS

- Regulatory/Commodity funds are separated as follows:

- Activities in these funds may have some of their own special rules from the State, dependent upon the type of fund, but for the most part, the same rules for General and State Line Item Appropriations apply.

- Regulatory funds are used for the collection of fees for fines or licensing regulated by the state of IN.

- Examples would be pesticide application licenses and fines or egg licenses.

- Commodities are used for the collection of state regulated fees for the sale of goods such as wine, mint, and wool.

- Regulatory Funds are separated as follows:

- 33010009 – Office of the Indiana State Chemist (OISC)

- 36010000 – Restricted – Other

- Funded Program Type: Restricted Commodity

- Includes what used to be:

- 3302XXXX – Commodity

- 3305XXXX – AES Public Service

- Funded Program Type: Restricted Regulatory

- Includes what used to be:

- 3301XXXX – Regulatory

- 3310XXXX – Regulatory Supported Research

- This fund is not limited to commodity and regulatory, but will include them

OTHER COMMON AG FUNDS

- Other common Ag funds are separated as follows:

- 21020000 – General Fund

- Funded Program Type: General Extension

- Includes what used to be:

- 3205XXXX – Publications

- Funded Program Type: Income Producing – Digital Education/Conferences

- Institutional Attribute – Conference

- Includes what used to be:

- 2212XXXX – Income Producing Agriculture (Workshop)

- 36010000 – Restricted – Other

- Funded Program Type: Restricted – Other

- Includes what used to be:

- 3205XXXX – County Extension Billing

COUNTY APPROPRIATIONS

- County appropriations are changing from 3201XXXX to 36010000 with the Funded Program Type Restricted – County Extension.

- Purdue receives funds from the county governments to support Extension Educators within each county.

- The educators are Purdue employees and are the liaisons between the Extension Specialists on campus and the general public.

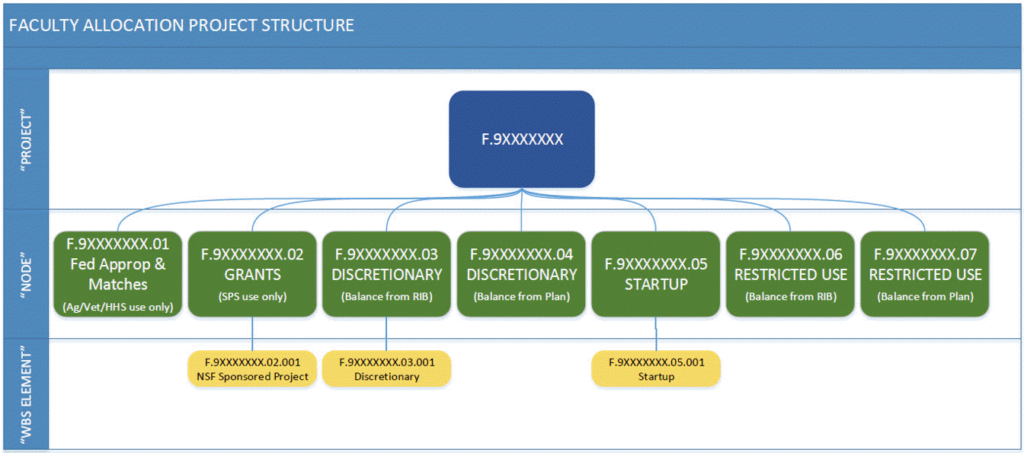

WBSE – FACULTY ALLOCATION STRUCTURE

- Node 1 of the Faculty Allocation Structure is reserved for Ag/Vet/HHS use only.

- This is where expenses for salary on federal and matching funds is tracked by project for the Federal Appropriation reporting.

- When viewing allocations, faculty will not see Node 1.

- Business Offices can run a custom SAP report (TBD) to view all Node 1 entries and balances.

- Discretionary Node’s 3 and 4 should never be used with Federal funds.

- Node 1 will be used for setting up any salary accounts, as mentioned in the previous slide.

- Use Node 5 for Start-Up accounts regardless of fund.

- All other accounts on federal appropriated funds should be set up in Restricted Node’s 6 or 7.

- Unless marked as an Internal Award, all WBSE accounts on State Line funds should be listed in Discretionary Nodes 3 or 4.

AG AND STATELINE FEDERAL APPROPRIATIONS

Federal appropriation categories, allowable expenditures and WBSE – Faculty Allocations

FEDERAL APPROPRIATIONS

- Federal Appropriations are separated by mission:

- 3401XXXX – Extension

- 3451XXXX – Research

- Direct costs to these funds must be allowable, allocable, and reasonable.

- These funds are governed by Uniform Guidance

FEDERAL APPROPRIATIONS: SMITH LEVER – 3401XXXX

- The Smith-Lever Act of 1914 established the Cooperative Extension Service in each state.

- Only individuals with extension appointments can expend these funds.

- Expenditures must be in furtherance of the Extension mission covered in the annual Plan of Work.

- Funds are divided as follows:

- 34010000 – Smith Lever

- 34010002/34010003 – Expanded Food and Nutrition Education Program (EFNEP)

- 34010004 – Renewable Resources Extension Act (RREA)

FEDERAL APPROPRIATIONS: HATCH APPROPRIATIONS – 3451XXXX

- The Hatch Act of 1887 was enacted to provide research funding on all aspects of agriculture.

- Funds are divided as follows:

- 34510000 – Hatch

- 34510001 – Multistate Research

- 34510002 – Animal Health

- 34510003 – McIntire Stennis

- PIs with a 20% or more research appointment are required to have a Hatch project.

- Only those PIs with approved Hatch projects can utilize these funds.

- Hatch Appropriations – CRIS 419 Report

- CRIS 419 reports expenditures on all National Institute of Food and Agriculture (NIFA) approved research projects for the federal fiscal year.

- The report assumes the work being done benefits the Hatch, Multi-State, Animal Health, or McIntire Stennis funds.

- Support personnel and graduate students assigned to a faculty member should use the faculty member’s WBSE number.

- Expenses cannot be adjusted on these funds after the close of the federal fiscal year (September 30).

- Hatch Appropriations – CRIS 419 Report

FEDERAL APPROPRIATIONS: ALLOWABLE EXPENDITURES

| CHARGEABLE | |

| Prospective Employee Travel | |

| Publications | |

| Capital Expenditures | With prior NIFA approval. |

| General Purpose Equipment | Computers, farm machinery and equipment (greater than $5000 requires approval). |

| Special Purpose Equipment | Scientific or research equipment (greater than $150,000 requires approval). |

| General S&E Costs | If directly associated with project and is allocable, reasonable, and allowable under Uniform Guidance. |

| Payroll | Faculty members and those they directly supervise working on approved projects. |

| Conferences and Workshops | Primary purpose must be to spread technical information. Covers rentals, speaker fees, local transportation, meals and refreshments (usually not breakfast or dinner). |

| Travel | Smith-Lever requires prior USDA approval for foreign travel. Hatch requires Director approval for both foreign and domestic travel. |

| Extension Employee Moving Costs | |

FEDERAL APPROPRIATIONS: UNALLOWABLE EXPENDITURES

| NOT CHARGEABLE | |

| Hospitality | |

| Entertainment | |

| Promotional Items | |

| Fines and Penalties | |

| Lobbying | |

| Tuition and Fee Remission | |

| Payroll | No clerical/service or administrative/management unless unlike circumstance can be provided. Typically not allowed because the time is not dedicated solely to one purpose.Department Heads should be paid on State Line Item Funds or General Funds. Lobbying issues could exist if paid on Federal Funds. |

| Memberships in Individual Names | |

| Building Purchase, Construction, Preservation or Renovation | |

| Purchase or Rental of Land | |

| Indirect Costs | |

| Cost Share | Federal funds cannot be used. |

WBSE – FACULTY ALLOCATIONS

- Node 1 of the Faculty Allocation Structure is reserved for Ag/Vet/HHS use only.

- This is where expenses for salary on federal and matching funds is tracked by project for the Federal Appropriation reporting.

- When viewing allocations, faculty will not see Node 1.

- Business Offices can run a custom SAP report (TBD) to view all Node 1 entries and balances.

- Discretionary Node’s 3 and 4 should never be used with Federal funds.

- Node 1 will be used for setting up any salary accounts, as mentioned in the previous slide.

- Use Node 5 for Start-Up accounts regardless of fund.

- All other accounts on federal appropriated funds should be set up in Restricted Node’s 6 or 7.

- Unless marked as an Internal Award, all WBSE accounts on State Line funds should be listed in Discretionary Nodes 3 or 4.

ANNUAL FINANCIAL AND COMPLIANCE LETTER

CARRYFORWARD

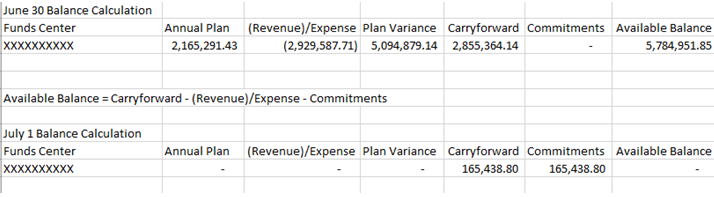

Available Balance Carryforward

This process will take place in two steps. Purchase order carryforward will occur the evening of June 30th, and the residual available balance carryforward will take place after June month end close as defined by the year end calendar.

Step One: Commitments

Any open Purchase Requisitions, Purchase Orders and Funds Commitment documents will automatically carryforward to the next fiscal year. This carryforward will occur at 12:01 a.m. July 1. No activity should occur on Purchase Orders until you receive communication via Business@Purdue from Accounting Services that activity can resume.

The commitment carryforward will carry forward both the commitment from the individual fund/funds center/funded program and commitment item as well as the appropriate available balance to cover that commitment.

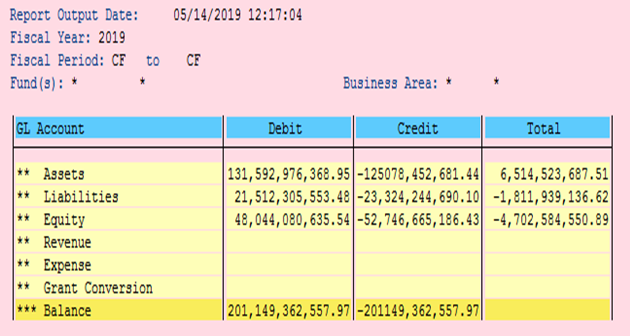

The example below shows the available balance calculation as of 6/30/20XX as it would appear in GR55 ZSFA.

After commitment carryforward has been completed the available balance will remain unchanged in the old fiscal year while the commitment and carryforward columns are reduced by the amount of commitments. In the new fiscal year, the carryforward and commitment columns will be equal and available balance will be zero.

Available balance in the new fiscal year will appear as zero until available balance carryforward is completed after month end close.

You can see the detail of commitment carryforward utilizing SAP Tcode FMEDDW with the following criteria:

| Budget Category: | 9F |

| Fiscal Year: | Current (New) Fiscal Year |

| Int. Bdgt. Process | CCF |

| Entry Doc. Type | CFWD |

| Fund: | Your Fund |

| Funds Center: | Your Funds Center |

| Funded Program: | Your Funded Program |

| Execute |

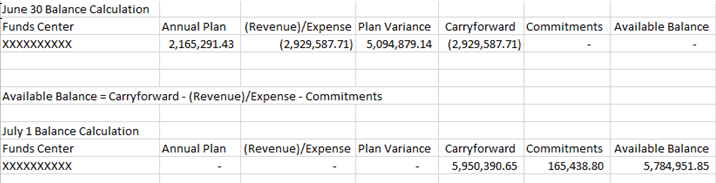

Step Two: Residual Available Balance Carryforward

Residual available balance carryforward will occur after June month end close at a date determined by Accounting Services. Please refer to the year end calendar for specific dates. Residual available balance carryforward moves the ending available balance from the old fiscal year to the new fiscal year at the funded program level with the carryforward amount posting on commitment item 520000 in the new fiscal year, or in cases where parent/child relationships have been defined from the child account to the parent account.

In the old fiscal year the carryforward amount is reduced by the available balance, bringing the available balance calculation to zero. In the new fiscal year, the carryforward amount is increased by the available balance, bringing the entire available balance forward into the new year.

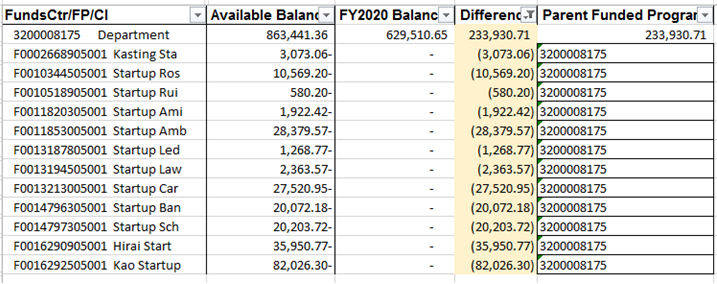

The available balance in the new year should match the available balance from the old year except for those that have been defined as having parent/child relationships. For accounts that have a defined parent, the carryforward of the available balance at the end of the year rolls up to the account that has been defined as the parent as shown in the example below.

Account 3200008175 has been defined as the parent for all of the Start-Up accounts within the department. These accounts have a total negative available balance of $233,930.71. The parent account has an available balance of $863,441.36, but is reduced by the negative child balances to $629,510.65 (863,441.36 – 233,930.71 = 629,510.65)

You can also find the detail of the residual available balance carryforward using SAP tcode FMEDDW with the following criteria.

| Budget Category: | 9F |

| Fiscal Year: | Current (New) Fiscal Year |

| Int. Bdgt. Process | CORV (Carryforward Receiver) |

| Entry Doc. Type | CFWD |

| Fund: | Your Fund |

| Funds Center: | Your Funds Center |

| Funded Program: | Your Funded Program |

| Execute |

Balance Sheet Carryforward

For all funds, all 4xxxxx and 5xxxxx g/l’s will close to 300001 g/l. When executing GR55 / Z100 report, use period 0 to display your carryforward balances.

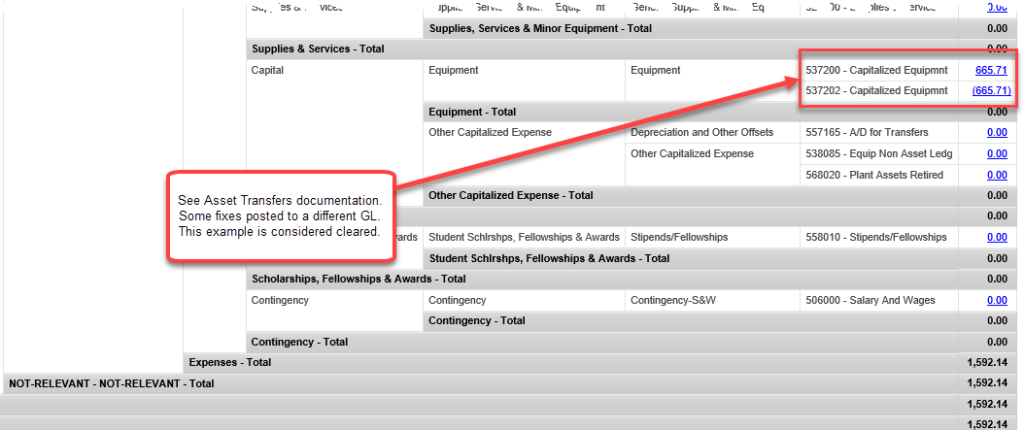

CLEARING NOT-RELEVANT FUNDED PROGRAM POSTINGS PROCESS

With the FY 2019 transformation project implementation, there should no longer be any postings to NOT-RELEVANT Funded Programs. All transactions should include an Order or WBSE which will flow into the Funded Program field. The expectation is that NOT-RELEVANT balances will be cleared on a monthly basis.

This document will show current resources that can be used to review these balances and fix any postings that have occurred.

PROCESS

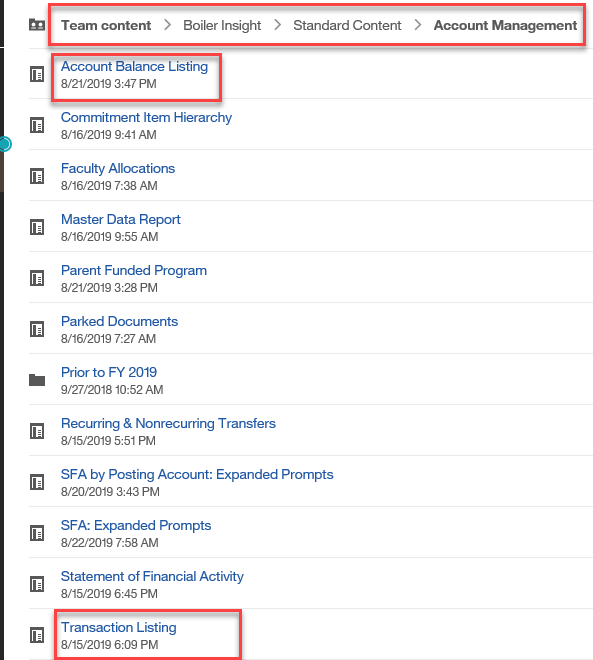

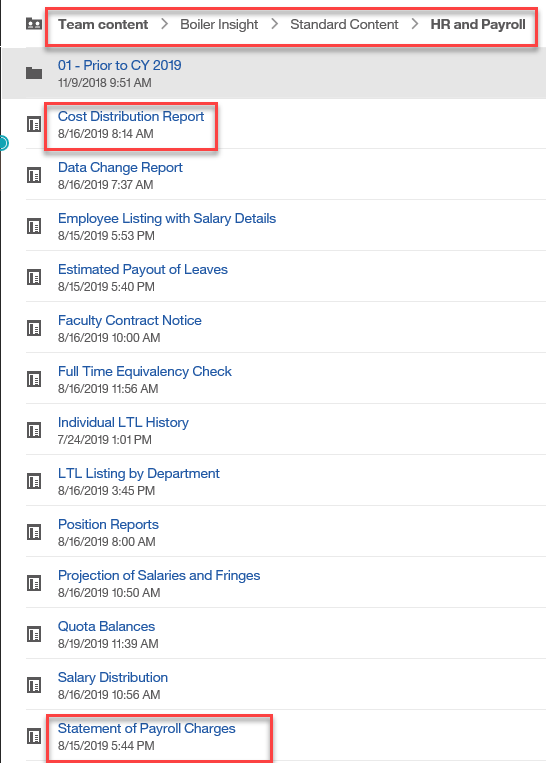

- Review one of the Cost Distribution Reports before each payroll to ensure nothing is set to post to NOT-RELEVANT.

- Identify outstanding NOT-RELEVANT balances by using one of the Account Balance Listing reports or the Transaction Listing (summary version), shown below in Resources, to identify balances.

- Process correcting documents or IT27 changes to clear balances.

- If process that created the posting is recurring, work with process owners to fix the process.

BEST PRACTICES

- Be sure newly hired staff have cost distributions set up in IT27. Use Data Change Report or Data Change Schedule Version report to identify newly hired staff.

- Be sure to fix the source system so recurring NOT-RELEVANT charges do not take place.

| Type of Posting | Method to Correct | Notes |

| S & W/ Fringe Benefits | ECP – IT27 | Fix the Salary and Fringe Benefits should follow. |

| Assets | Change In Asset Funding Form | |

| WIP | Contact Physical Facilities | AOBOacct@purdue.edu |

| Travel | Concur | Ensure account assignments are identified and reports approved |

- Work with Property Accounting on Asset Transfer balances.

- B@P News Article: Asset transfers will reflect differently on financial reports for FY 2019

- Complete Change In Asset Funding form

- WIP Charges – charges if the departments are being charged on Not-Relevant they need to be contacting Sherry McQueary ( AOBOacct@purdue.edu) to get the settlement receiver changed.

- Be aware that Unreconciled Travel Card transactions are now being accrued on a monthly basis. These transactions are hitting Commitment Item 535110 (In-State Travel, Period 2019-02) or 546417 (Travel Card Charges, 2019-03 on) on the NOT-RELEVANT Funded Program. These charges will automatically reverse themselves in the next month. To help reduce the amount hitting not-relevant each month, travelers should be reconciling expense reports within 30 days of travel. Contact Janessa Martin with questions.

RESOURCES

REVIEW BALANCES & IDENTIFY TRANSACTIONS

Users may choose to use either of the following reports to begin researching their NOT-RELEVANT balances.

- Account Balance Listing or Account Balance Listing Scheduled View

- Select Funds Management – Details Version (for non-scheduled view select HTML version so drill thru hyperlinks are active)

- Time & Fund Prompts: Run for current period

- Funds Center Prompts: Select a Funds Center, Business Area, etc.

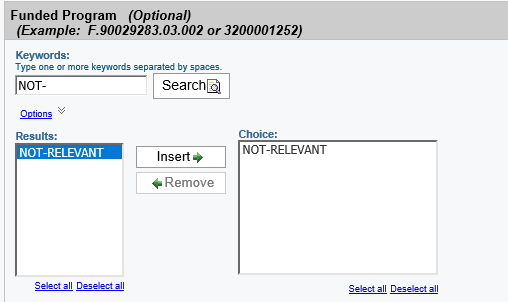

- Funded Program Prompts: Search and select Funded Program = NOT-RELEVANT

- Submit

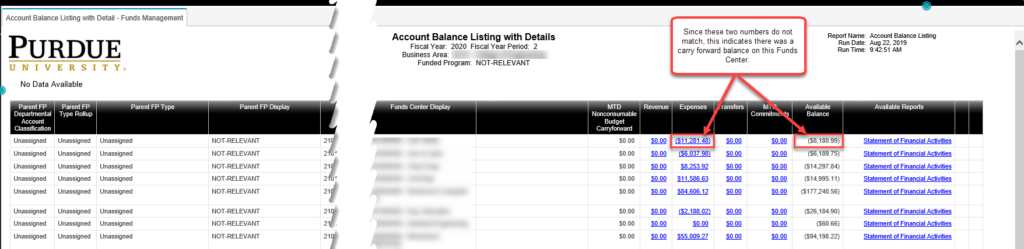

- Drill thru’s can be used to get transactions for the current fiscal year. If Funds Center had a Carry Forward Balance on NOT-RELEVANT, use Transaction Listing to see all transactions.

- If there were Carry Forward Balances, use Transaction Listing to get a full list of outstanding transactions.

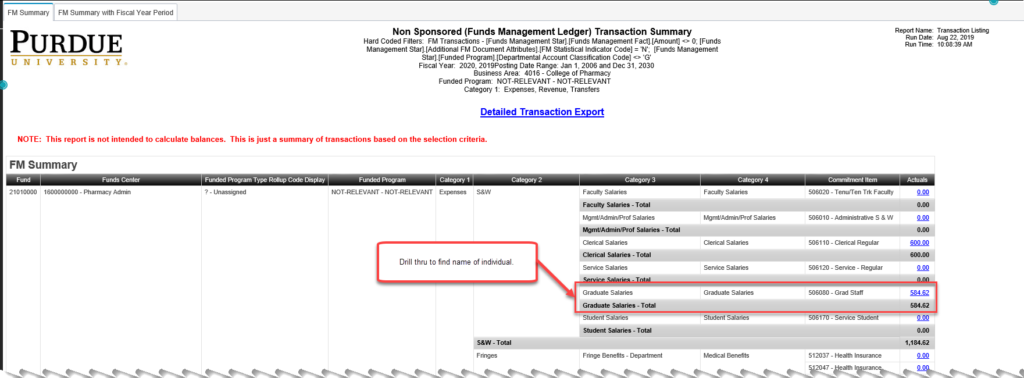

- Transaction Listing

- Select Non Sponsored (Funds Management Ledger) Report

- Time & Fund Prompts: Control>Click to select Fiscal Years 2019 & 2020

- Funds Center Prompts: Select a Funds Center, Business Area, etc.

- Funded Program Prompts: Search and select Funded Program = NOT-RELEVANT

- Submit

- Use drill thru reports to review detailed transactions to see what needs to be fixed

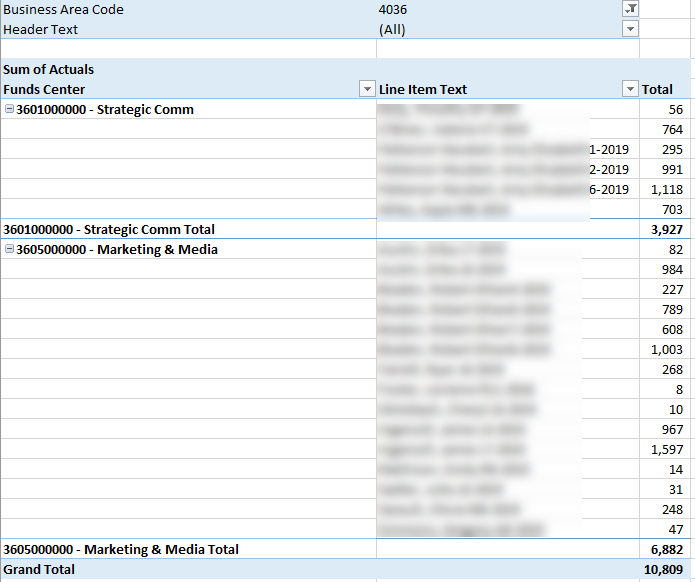

- To find unreconciled travel, run an export version of the Transaction Listing on NOT-RELEVANT for your Funds Center and 546417 (after 2019-03). Create a pivot on the Line Item Text, which shows the travelers name.

RESEARCH POSTINGS

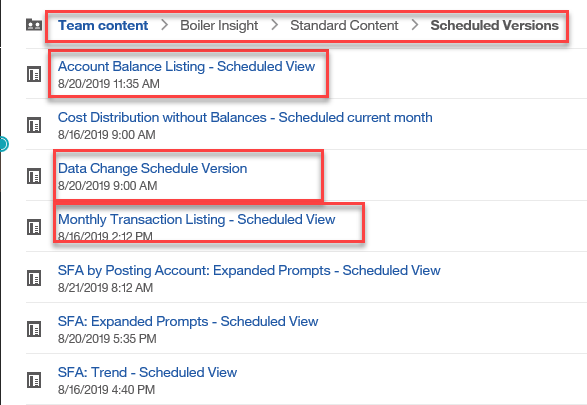

- Transaction Listing or Monthly Transaction Listing – Scheduled View

- See notes above for running instructions

- Statement of Payroll Charges

- Time & Fund Prompts: Control>Click to select Fiscal Years 2019 & 2020

- Funds Center Prompts: Select a Funds Center, Business Area, etc.

- Funded Program Prompts: Search and select Funded Program = NOT-RELEVANT

- Submit

- NOTE: If charges do not run through the payroll system (Direct Invoice Vouchers, JV’s, etc.) the postings will not show in this report.

NOT-RELEVANT POSTING PREVENTION

- Data Change Report or Data Change Schedule Version

- Identify new staff that need Cost Distribution set up

- Cost Distribution Report or Cost Distribution without Balances – Scheduled current month

- Review Cost Distributions on NOT-RELEVANT

REPORT PATHS

DOCUMENT TYPES

Listing of all document types.

FISCAL APPROVAL WORKFLOW

All transactions should be reviewed for allowability, allocability and reasonableness, regardless if it is routed for fiscal approval or auto-approved through SAP. Business Office staff should work with initiators and requesters to ensure they understand the basics of allowability, allocability and reasonableness. The following information defines fiscal approval, workflow and walks through specific transactions.

FISCAL APPROVAL TABLE

- The table is by position number so when there is turn over nothing is changed in the table. When changes are made to the table the position and level are reviewed to ensure they are appropriate.

- Best practice is to have 2 approvers at each of the Fund Center Levels 1-3.

- To make changes to the Fiscal Approval Table use the Master Data SharePoint site at the link below.

- Master Data SharePoint – West Lafayette

The following table outlines the Fiscal Approval Levels and how they are used:

| LEVEL | $ LIMITS | BUSINESS AREA OR FUND CENTER | APPROPRIATE POSITION TYPE FOR LEVEL | System |

| 0 | 1,000 OR LESS | N/A | Ariba, ZV60 KR , FV50 SA, Concur | |

| 1 | $1,001 – $5,000 | Fund Center | Account Clerk/Assistant or higher | Ariba, ZV60 KR , FV50 SA, Concur |

| 2 | $5,001 – $25,000 | Fund Center | Business Manager or higher | Ariba, ZV60 KR , FV50 SA, Concur, Property Accounting |

| 3 | $25,001 – $100,000 | Fund Center | ADFA/DFA or higher Also a “Large School” Business Managers may also have this authority | Ariba, ZV60 KR , FV50 SA |

| 3 | 25,001 or higher | Fund Center | ADFA/DFA or higher Also a “Large School” Business Managers may also have this authority | Concur |

| 3 | Preauditor | Business Area | Designated preauditor person – To be a designatedPreauditor the person needs to take the Preauditortraining | FV50 SA |

| 4 | $100,001 – $500,000 | Fund Center | Senior DFA or Vice Chancellor Fiscal Affairs | ZV60 KR |

| 4 | $100,001 – $500,000 | Fund Center | Senior DFA or Vice Chancellor Fiscal Affairs | Ariba |

| 5 | $500,001- $1,000,000 | N/A | Assistant Treasurer | Ariba and ZV60 KR |

| 6 | $1,000,001- $2,000,000 | N/A | Treasurer | Ariba and ZV60 KR |

| 7 | $2,000,001 or higher | N/A | BOT however it routes to the Treasurer and then the Treasurer takes it to the Board. | Ariba and ZV60 KR |

*Ariba and Concur changes level at 1000.01, 5000.01, etc. and SAP changes levels at 1001.00, 5001.00 etc.

BA LEVEL 3

- The BA level 3 is considered the Preauditor and the Preauditor should attend the preaudit training before being placed in this level. Because this level approves balance sheet transactions some exceptions have been made to areas that do not have many grant funds. Contact Master Data team if you feel you have this situation.

- This level will approve FV50’s with grants and federal funds included in the document.

- This level will also approvers balance sheet transactions. Balance sheet transactions are defined as a document where there are no WBSE or IO’s.

TRANSACTIONS WHICH USE FISCAL APPROVAL

- Direct Invoice Voucher – ZV60 KR

- Journal Voucher – FV50 SA

- Purchasing – Ariba Purchase Orders

- Concur – PCard/TCard Reconciliations

- Concur – Travel Approvals

- Property Accounting Documents

DIRECT INVOICE VOUCHERS (DIV)

- Will be initiated via SAP ZV60 transaction only

- Initiator role limited to Business Office/Central staff only

- KR doc type transactions will route for fiscal approvals

- Tax reviews all payments to vendors not coded as corporate, government or tax-exempt

- If vendor’s Recipient Type is blank, payment will route to Tax for review and updating

- Transactions > $1,000 routed electronically for required fiscal approval

- Initiator cannot approve their own transactions

- Transactions > $5,000 will skip the level 1 approver

- Transactions > $25,000 will skip level 1 and 2 approvers

- Total invoice amount will determine approver level for all cost centers involved.

- If more than one cost center or BA, will route to approver for each unit at total invoice level

- If the invoice is for more than $100,000 it will route to level 3 first and then stop at each level after until it is approved by the highest level needed for the amount. Example: If the payment is for 900K it will route to Level 3, 4, and 5 before it is approved.

- Process designed to allow previously approved contract payments to bypass workflow

- ZV60 initiators need to complete the ZV60 training

JOURNAL VOUCHERS (JV) SA DOCUMENT TYPE

- Will be initiated via FV50 transaction only

- SA doc type transactions will route for fiscal approvals

- Uses same approver table as external transactions

- Total debits/credits determine approver level

- All cost centers impacted will approve

- “Skips” to final approval level

- Will not route above level 3

- Initiators cannot approve their own JV’s

- SA docs with grant accounts will always route directly to BA level 3 approver for pre-audit approval.

- Journal vouchers with balance sheet transactions which are defined as transactions with only the BA and no Order or WBSE will route to the BA level 3. If the document has a line that does include an Order or WBSE it will route to the approver associate with the cost center at the appropriate level.

- Journal vouchers with Ag federal funds included will also route to the BA level. At this time not all federal funds are routing properly but this is being investigated.

PURCHASING – ARIBA PURCHASE ORDERS

- Requisitions $1,000 and less will not route for approval

- Requisitions > $1,000 will route for approval and it will not skip any levels

- Example: A requisition for $27,000 will stop at Level 1, 2 and 3

- Other special approvals currently in use will also be in the approval flow

CONCUR – PCARD/TCARD RECONCILIATIONS

- Document Type PC –Procurement Card and TC – Travel Card

- If T-Card and P-Card reports have any charges that are over $1000 they will route to the level 1 approver. If all the charges on the report are less then $1000 is will not route for approval.

- Transactions > $1,000 will require fiscal approval

- The reconciler approval will follow the Concur workflow

- Level 1 $1,001 – $5,000

- Level 2 $5,001 – $25,000

- Level 3 > $25,000

- Only 1 Concur approver can be marked at each level for each Responsible Cost Center (RCC)

- Link for Purchasing Card Policies and Procedures

CONCUR – TRAVEL APPROVALS

- Travel report approvals are split between small and large approver and is marked on the approver table at the Level 1 or the level 2 Cost Center.

- Small approver is level 1 for up to $5,000

- Large approver is level 2 for over $5,000

- Only 1 Concur approver can be marked at each level for each Responsible Cost Center (RCC)

PROPERTY ACCOUNTING DOCUMENTS

- Property accounting forms completed via the Finance Launchpad in the OnePurdue portal.

- All property accounting forms will route to the level 2 fiscal approver.

- The property accounting forms include:

- Cannibalize an asset

- Change in location of an asset

- Donation of an asset

- Inventory reconciliation

- Property off campus

- Send to WL warehouse

- Transfer ownership

- Stolen asset

- Transfer out of Purdue

- Change in asset funding

- Link for Property Accounting

OTHER SAP FINANCIAL DOCUMENTS

- Grant Subcontract Payments are processed via ZV60 but are XR documents so they do not use the workflow fiscal approver table. It is approved by the SPS account manager and the PI

- Intramural Invoice Voucher (IIV) Tcode FV50 document type JN and various other financial document types will not route through workflow

- Users will continue existing process except that backup documentation will be attached electronically by the user rather than routed on paper

- Preparers should NOT approve their own documents

INCOME PRODUCING OPERATIONS

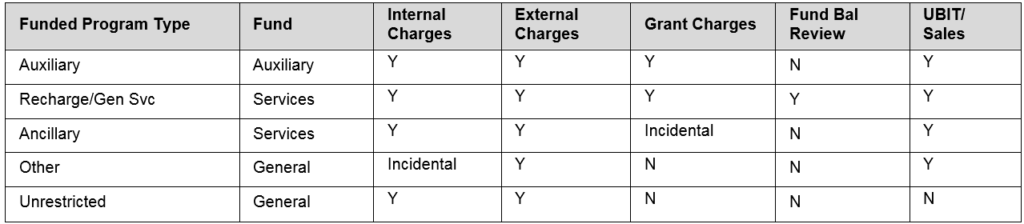

DEFINITIONS

| Activity | Definition |

|---|---|

| Recharge/General Service Centers | Sales of goods and services necessary for University operations primarily between internal customers; however, can also have sales to external customers. |

| Ancillary | Activities that charge fees; however, exist primarily to provide a practical learning experience for students in furtherance of core University missions of Learning, Research, and Engagement. |

| Auxiliary | Sales of optional or convenience goods and services to primarily students and employees, or secondarily to the general public. Primary purpose is something other than providing a practical learning experience for students that counts towards their degree programs. General expectation of financial self-sufficiency for the auxiliary organization as a whole including overhead costs. |

| Other | Operations that charge primarily external customers and need reviewed periodically for UBIT or Sales Tax liability. |

| Unrestricted | Income producing activities that do not require distinct accounting and reporting due to Federal and State regulations including UG and Tax Laws. Examples: Digital Ed, Study Abroad, Copy Charges, PUSH, etc. |

STRUCTURE

EXTERNAL REGULATIONS

- Policies and practices must reflect government regulatory costing and accounting principles which are required by:

- The Code of Federal Regulations 2 CFR 200, also known as Uniform Guidance

- Costing Principles required by the Cost Accounting Standards Board

- Federal and State Tax Regulations

KEY FEATURES

- While goods and services could in some cases be purchased from commercial sources, for reasons of convenience, cost and/or control, the good or service is often provided more effectively through an income producing operation.

- The activities can either be ongoing or one-time.

- All appropriate internal controls for cash, inventory and accounts receivables must be followed.

- Policies and procedures have been established to provide consistent operational practices among the various income producing operations and to ensure compliance with governmental regulations.

RECHARGE /GENERAL SERVICE CENTERS

- Recharge and General Service Centers use Internal Services Fund 22500000 and the Funded Program Type ‘Income Producing – Recharge’.

- Customers are primarily University departments; however, can have external customers.

- Goods and services provided are necessary for University operations.

- Rates are calculated and maintained in a manner appropriate for charging grants.

- Items that are specifically restricted by the federal government under 2 CFR Part 200, Cost Principles under Uniform Guidance, may not be charged.

- Internal rates for goods and services must be computed at the break-even by estimating the full direct cost of the activity for the upcoming period including any accumulated surplus or deficit from prior year operations.

- Centers must not generate an operating surplus on internal charges (including grants); however, subsidization of rates may be appropriate in some cases.

- Sales to external customers must be at least breakeven plus F&A; however, market rates can be charged to external customers

- Rates must be reviewed for market competition, UBIT (Unrelated Business Income Tax) and sales tax issues.

- Examples of centers include:

- Core Research Facilities (Birck, Prime Lab, Electron Microscopy, etc.)

- Animal Care Facilities

- Transportation

- Benefits

- Risk Management

- All associated revenues and expenses for the operation must post to the IO.

- The full direct cost of the recharge center activity should be incurred in the recharge center IO and subsequently included in the charge rates.

DEPRECIATION RECOVERY

- Depreciation recovery will be done by reducing the revenue-increasing-budget balance.

- This budget amount will be reposted to the account on a ‘Non-Consumable’ budget type, which will prevent the depreciation recovery from showing in the account balance.

- When the recovery funds need spent, an FMBB can be processed to reclassify the necessary funding as ‘Consumable’.

ANCILLARY

- Ancillary activities use Internal Services Fund 22500000 and the Funded Program Type ‘Income Producing – Ancillary’.

- Activities that charge fees; however, exist primarily to provide a practical learning experience for students in furtherance of core University missions of Learning, Research, and Engagement. For example:

- Vet Hospital

- Speech and Language Clinics

- Nursing Clinics

- Pharmacy

- Ismail Center

- HTM

- Meat Lab

- Customers can be internal or external.

- Ancillary activities can generate an operating surplus or require subsidies to operate.

- Rates must be reviewed for market competition and sales tax issues.

- Rates are appropriate only for incidental charging of grants.

- Associated revenues and expenses for the operation must post to the IO.

AUXILIARY

- Uses Auxiliary Fund 24500000 and Funded Program type ‘Income Producing – Auxiliary.’

- Provides optional or convenience goods and services for which customers are primarily students and employees (or secondarily to the general public) rather than University departments.

- Primary purpose of the activity is something other than providing a practical learning experience for students that counts toward their degree programs.

- General expectation of financial self-sufficiency for the auxiliary organization as a whole including overhead costs.

- Activities that charge grants more than incidentally should not be in Auxiliary.

- Auxiliary activities can generate an operating surplus.

- All associated revenues and expenses for the operation must post to the Internal Order.

- Activities primarily include:

- Athletics

- Student Housing & Dining

OTHER

- Other Income Producing Activities use General Fund 21010000* and the Funded Program Type ‘Income Producing – Other’.

- Operations that charge primarily external customers and need reviewed periodically for UBIT (Unrelated Business Income Tax) or Sales Tax liability.

- All associated revenues and expenses for the operation must post to the Internal Order.

- The activities can generate an operating surplus; however the surplus would need to be transferred out if it is spent on activities un-related to this.

- Grants cannot be charged.

- Rates must be reviewed for market competition and other issues.

- Agriculture can also use funds 21030000 and 21020000

- Convocations, Bands, PMO, Rec & Wellness for specific rates that have UBIT issues

- If UBIT unlikely, rates revenue can post to general fund

UNRESTRICTED

- Uses General Fund 21010000 and the Funded Program Type ‘Unrestricted to Department’.

- Some activities may be identified with an Institutional Attribute of ‘Digital Education – For Credit’.

- Income producing activities that do not require distinct accounting and reporting due to Federal or State regulations including Uniform Guidance, tax laws or other regulations – use of the funds is unrestricted

- Agriculture can also use funds 21030000 and 21020000

- Activities include:

- Digital Education

- Conferences

- Study Abroad

- Misc. Course Fees

- Publications

- Copy Charges

- PUSH/CAPS

- Material Testing Agreements

DELIVERABLES

- Efficiency and consistency in advising, developing, and monitoring rates due to expertise in cost accounting and rate development.

- Clear and consistent definitions and governance for Internal Service Centers, Auxiliary, Ancillary, and Other Income Producing Activities.

- A revised accounting structure which will allow for clear identification of each type of activity for enhanced reporting and simplified monitoring procedures that is adapted to limit the governance to what is required for each of the activities.

SERVICES

- Rate Consulting & Creation

- Provide expertise and advice to the Facility Director and Business Office Financial Manager to determine the need for a rate.

- Rate Creation

- Gather information from the Facility Director and Business Office Financial Manager to prepare the rate request documentation. Approval from the Dean or Department Head authorizing financial support of the recharge or general service center and then approval from the Senior Vice President and Assistant Treasurer or their delegate will be required before the rate is put into place.

- Rate Maintenance and Monitoring

- Although the departmental Business Office will be responsible for the financial management of the center, the Rate/Recharge Shared Service Center will conduct an Annual Fund Balance Review and periodic detailed review of recharge and general service center rates and practices along with setting minimum timelines to update rates.

- Study Abroad

- The Rate/Recharge Shared Service Center rate review after approval by Dean or Department Head authorizing support of the activity and Senior Director – Comptroller or their delegate.

- Delegated Rates

- Provide guidance to the following areas that continue to have delegated rate setting approval: Digital Education, Excess Agriculture Commodities, Conferences, Convocations, WBAA Underwriting Rates, and Athletics. The state legislature and commodity boards set the Ag Commodity rates not the University. Only the Ag Workshops do not go through conferences.

- Regional Campuses

- Currently the Regional Vice Chancellor for Financial and Administrative Affairs has been delegated approval; however, a process will be developed to allow for rate creation, maintenance and monitoring that includes the service center.

- Tuition or University Residences Room and Board Rates

- The service center will not initially include advising, monitoring, or developing rates for these areas.

INTERNAL GRANTS

- Internally funded grants are included in the Faculty Allocation structure and not in the Grants Management (GM) module. This provides transparency, consistency and reporting.

- Institutional Attribute of IG – Internal Grant will be used to track internal awards. Internal awards are designated as “operating funds” including awards funded by the Provost, EVPRP, and Graduate School (as well as awards from departments, schools, and colleges), to be administered consistently.

- Other faculty accounts should be designated as internal grants if they meet the following definition:

- Allocations made to faculty members from departmental, college or university funds to support specific research projects or equipment required for research are internal grants. Typically, internal grant allocations are received by faculty either after responding to an internal solicitation for project proposals or after requesting funding for a specific project. Discretionary allocations, which the faculty member decides to use for research activities, should not be classified as internal grants.

LEASES

The Governmental Accounting Standards Board (GASB) establishes accounting and financial reporting standards for U.S. state and local governments that follow Generally Accepted Accounting Principles (GAAP). Purdue University must comply with GASB standards for financial reporting purposes. GASB has released a new standard titled “GASB 87 Leases,” which includes significant changes to how leases must be recorded. This Statement establishes standards of accounting and financial reporting for leases by lessees and lessors. The requirements of this Statement apply to financial statements of Purdue University.

LEASE DEFINITION

For purposes of applying this Statement, a lease is defined as a contract that conveys control of the right to use another entity’s non-financial asset (the underlying asset) as specified in the contract for a period of time in an exchange or exchange-like transaction. As used in the definition of a lease, a non-financial asset includes land, buildings, vehicles, and equipment.

To determine whether a contract conveys control of the right to use the underlying asset, a government should assess whether it has both of the following:

- The right to obtain the present service capacity from use of the underlying asset as specified in the contract

- The right to determine the nature and manner of use of the underlying asset as specified in the contract.

Leases include contracts that, although not explicitly identified as leases, meet the definition of a lease. This definition excludes contracts for services except those contracts where an embedded lease is included. An embedded lease is a lease component within a larger contract.

For example, a company could enter into an arrangement with an information technology organization to host its data on a dedicated server. Embedded within this IT hosting arrangement may be the company’s right to direct the use of a specified server, which may meet the definition of a lease.

If you are unsure if your contract contains an embedded lease component, or applies to this standard, please contact Accounting Services at accountingservices@purdue.edu.

LESSEE JOURNAL ENTRIES

If we are the Lessee then we have contracted with another party to lease a right to use asset. The department will expense the lease payments. Central Accounting will then record the right to use assets. In these instances we are required to record those right to use assets on our books and appropriately amortize them. In addition amortize the net present value of the lease liability we have entered into. Below is an example of the entries that would need to be made.

BUSINESS OFFICE LESSEE JOURNAL ENTRIES

Business Office Lessee Journal Entry

| Debit | Credit | |

| Lease/Rental Expense (see list below) | XXX | |

| Vendor/Accounts Payable | XXX |

| Commitment Item | Long Name | Description |

| 532030 | Rent-Non-cap.Computing Eq | Expenses for rentals and maintenance of computing equipment |

| 532005 | Building Rental | Expense for rented space related to leases or contract payments; not to be used for space rental for events |

| 532010 | Land Rental | Expense for land rental payments |

| 532015 | Space Rental | Expense for rental of space for not lease related space; primarily used for events |

| 532040 | Rent-Other Non-cap.Equip. | Expense for rentals and maintenance of equipment of other non capital items including artwork |

| 532055 | Rent-Other Cap. Equipment | Expense for rentals of capital equipment and machinery |

CENTRAL OFFICE LESSEE JOURNAL ENTRIES

Central Office Lessee Journal Entry

| Debit | Credit | |

| Lease Asset | XX,XXX | |

| Lease Liability | XX,XXX |

Central Office Lessee Subsequent Journal Entry

| Debit | Credit | |

| Lease Liability | X,XXX | |

| Amortization Expense | X,XXX | |

| Interest Expense | XXX | |

| Lease/Rental Expense (offset business office expense) | X,XXX | |

| Accumulated Amortization | X,XXX |

LESSOR JOURNAL ENTRIES

If we lease one of our assets to another entity for use then we are the Lessor. In those situations, per GASB 87, we are required to record the lease receivables and deferred inflow of resources on our balance sheet.

BUSINESS OFFICE LESSOR JOURNAL ENTRIES

Business Office Lessor Journal Entry

| Debit | Credit | |

| Cash (Check-101014, Wire-101018) | XXX | |

| Lease/Rental Income (see list below) | XXX |

| Commitment Item | Long Name | Description |

| 422900 | External Income – Other Rental Income | Revenue from external customers that would be renting property long term |

CENTRAL OFFICE LESSOR JOURNAL ENTRIES

Central Office Lessor Journal Entry

| Debit | Credit | |

| Lease Receivable | XX,XXX | |

| Deferred Inflow of Resources | XX,XXX |

Central Office Lessor Subsequent Journal Entry

| Debit | Credit | |

| Lease/Rental Income (offset business office income) | X,XXX | |

| Deferred Inflow of Resources | X,XXX | |

| Lease Receivable | X,XXX | |

| Interest Income | XXX |

QUICK REFERENCE GUIDE

RESERVES AND EARMARKS

RESERVES

Reserves are funds set aside separate and apart from an operating budget over time to invest in, maintain, or replace facilities or equipment, to support strategic programs and initiatives, or as a contingency for unplanned expenditures.

The categories used to identify reserve internal orders (via the Department Account Classification (DAC) field) are:

- Capital: Reserves specifically for new buildings or capital renovations

- Equipment: Reserves for capital equipment purchases (either replacing existing equipment or investing in new capabilities) or maintenance

- R&R: Reserves for non-capital R&R projects

- General: All other reserve purposes not assignable to another category

- Institutional: Only to be used by Segment leaders (i.e. President, Provost, Treasurer, EVPRP, or regional equivalents)

Every “reserve” internal order (IO) has to be set up with a fund, cost center and DAC attribute. There are five DAC’s representing the five reserve categories. See “Level and specific requirements” bullet below for more information regarding when, how many or what level reserve IO’s should be established.

Departmental Account Classification (DAC) attribute for:

- Capital Reserve*

- Capital Reserve is categorized as non-operating. Also note in the finance structure there is a Capital reserve DAC (includes projects not approved, future projects) and a Capital DAC (for projects that have been approved).

- Equipment Reserve

- Repair and Rehabilitation (R&R) Reserve

- General Reserve

- Institutional Reserve

Level and specific requirements in which reserves may be established:

- Capital Reserve – Internal Order (IO) may be established at Business Area level – this means an IO will be set up with an admin cost center (a financial unit).

- Funds held in Capital Reserve IO held at the admin cost center level may provide part of the funding for Capital Revenue IO’s that are set up at the financial unit cost center level (ie departmental level).

- Equipment Reserve – IO may be established for all cost centers.

- Repair and Rehabilitation Reserve – IO may be established at the financial unit cost center level (departmental level).

- This reserve could be used for startup funding that is not or has not been provided as a faculty allocation.

- General Reserve – IO may be established for all cost centers.

- No separate operating reserve for unfilled positions. However, units can transfer funds to general operating reserve at Business Area level (eg admin cost center).

- Institutional Reserve – IO may be established at Segment level – this means an IO will be set up. with an admin cost center (a financial unit) only at the Provost, EVPRP, President, TCFO areas and at equivalent level at PFW and PNW

- Institutional Reserves to be used for institutional goals and projects and may include internal grants.

Reserve internal orders should not have expenses posted directly to them. Funds should be transferred to a non-reserve account to be expensed.

EARMARKS

Establishing Earmarked Funds:

- Transaction code: FMZ1 – Create Funds Commitment

- A Funds Management (FM) earmark document with unique earmark number is created.

- User selects FM document type 11- Funds Commitment; system assigns value type 65 – Funds Commitment

- Available balance is reduced/committed.

- Unless have specific configuration, funds committed will continue in perpetuity if not relieved (ie will cross fiscal years).

- No commitments (earmarks, PO commitment, and parked document) flow through FI.

- A reconciling item between FI cash and FM available balance

Earmarks will be used on reserve IO’s. It is not a requirement to have earmarks on all reserves. Specifically,

- Capital Reserve – Use earmarks for each project.

- Equipment Reserve – Use of earmarks is up to the discretion of the unit.

- R&R Reserve – Use of earmarks is up to the discretion of the unit. Consider establishing earmark when a department commits to a future project, which has a specific timeframe, approved through a letter or with Dean’s approval.

- General Reserve – Use of earmarks is up to the discretion of the unit.

- Institutional Reserve – Use of earmarks is up to the discretion of the unit.

Outside of earmarks on reserves, earmarks will be used for contract payments. Contract payments use a restricted procurement document type that bypasses workflow for signature delegation.

- Relieving Earmarked Funds:

- Transaction code: FMZ2 – Change Funds Commitment

- Document transaction (such as JV (FV50)or invoice (FV60)) – earmark number is input into earmark funds field

- Reporting and Tracking Earmarks:

- Earmarks continue across fiscal years until relieved.

- Statement of Financial Activity (SFA) report (Standard Cognos report) – Recorded as a commitment on the SFA.

- SoFA Trend report (Excel based report) – Not recorded as a commitment on the SoFa Trend report.

RESTRICTED GIFT FUNDS (Gifts, Scholarships)

Funds received by the University with donor imposed limitations are restricted gift funds. Master data, definitions and procedures for the management and use of these funds can be found below.

Management guidelines for gifts defined as voluntary support can be found in the Voluntary Support section located at the bottom of this page.

MANAGEMENT GUIDELINES

Restricted gift funds received by the University from our donors provide crucial support for strategic programs across the university and require regular attention. Complying with donor intent through active use of the funds supports donor relations and incentivizes new donations through visible impacts.

Prioritizing the use of restricted gifts enables the University to preserve unrestricted funds for flexible use, including general operations, emerging priorities and unexpected contingencies.

Restricted Gift Fund Guidelines were published in October of 2025 and are intended to provide direction for ensuring the University fulfills its obligations to donors to timely and properly administer, manage, and spend its restricted gift funds.

All mention of “restricted gifts” in the guidelines document includes funds given with limitations on where they can be spent (university, college, department) but without restriction on what they are spent on (classified as unrestricted gifts) and those with restrictions on what they are spent on (classified as restricted gifts).

An overview of the guidelines as well as links to additional resources including the Restricted Gift Funds Scorecard are included below.

Overview

Charitable donations help ensure the University maintains its reputation for excellence in higher education and allows the University to fund programs, scholarships, fellowships, professorships, research, and facilities. These donations may be accompanied by restrictions that impose certain obligations on the University with respect to intended use, fiscal management, and reporting requirements, among other responsibilities. These donations may include gifts for current use as well as distributions from endowment gifts.

Gifts with restrictions must be used for purposes that are consistent with donor intentions. These intentions are typically detailed in a gift or pledge agreement, endowment agreement, or other types of documentation that are managed by Purdue for Life Foundation (PFLF) on behalf of the University. Departments with fiscal responsibility for restricted gift funds are expected to collaborate with PFLF to obtain the information or documentation needed to properly administer the funds in accordance with donor intent.

Timely Expenditures

Equally as important is ensuring restricted gift funds are spent in a timely manner. Accumulating these funds may not meet donor intentions and increases the risk of not being able to provide proper stewardship reporting. Restricted gift account balances should be reviewed at least twice per fiscal year to identify increasing or unspent balances. Once identified, a plan should be created to address the increasing or unspent balances, when appropriate. There may be unspent balances because of factors outside of a department’s control, such as unreasonable restrictions, which may require consulting PFLF for assistance. The Related Document, Forms and Tools section of this document includes a link to a reporting dashboard setup to assist with monitoring restricted gift accounts. Additionally, the Definitions section of this document outlines a description of what constitutes a well-managed account.

Donors may make contributions to provide the President, Dean, or Department Head restricted gift funds to be spent at their discretion. These contributions provide a great deal of flexibility and may be held in reserve for a reasonable period until projects are decided on and come to completion.

To allow for flexibility in the current and long-term financial planning of the University, departments should consider utilizing restricted gifts funds as one of the first sources of funding to support programs and activities meeting the restrictions. During the annual budget process, departments should consider material restricted gift funds that may be received over a multi-year term per the associated gift agreements.

Spend Appropriately

Approval of financial documents is required (purchase orders, travel requests, and direct pay vouchers, etc.) to ensure that the expenditure of restricted funds aligns with any applicable restrictions tied to the specific funds and supports the University’s purpose and mission. Additionally, it confirms that sufficient funds are available in the designated account(s). The approval must be granted by an authorized individual who is familiar with the account restrictions.

Donors may occasionally express preferences as to how their contributions are used, rather than restricting the funds. The University is not legally obligated to follow these preferences, but it is best practice to honor the preferences when possible, so long as the preferences continue to fit the needs of the benefiting area and the educational mission of the University.

Resources

These resources are maintained on the BPC Users SharePoint site (restricted). Access requests can be directed to cmdt@purdue.edu. Access to the Tableau Scorecard requires BI role PWL_320_bi_data_fi_level_1 and a consumer license.

Restricted Gift Funds Management Presentation (10.16.25)

Restricted Gift Funds Management Guidelines

GIFTS

The following outlines helpful information:

- University Gift Policy

- Restricted/Unrestricted/Designation and Funded Program Types

- Endowed and Non-Endowed Gifts

University Gift Policy

The policy outlines the responsible parties and definitions. University Gift Policy: http://www.purdue.edu/policies/business-finance/iib2.html

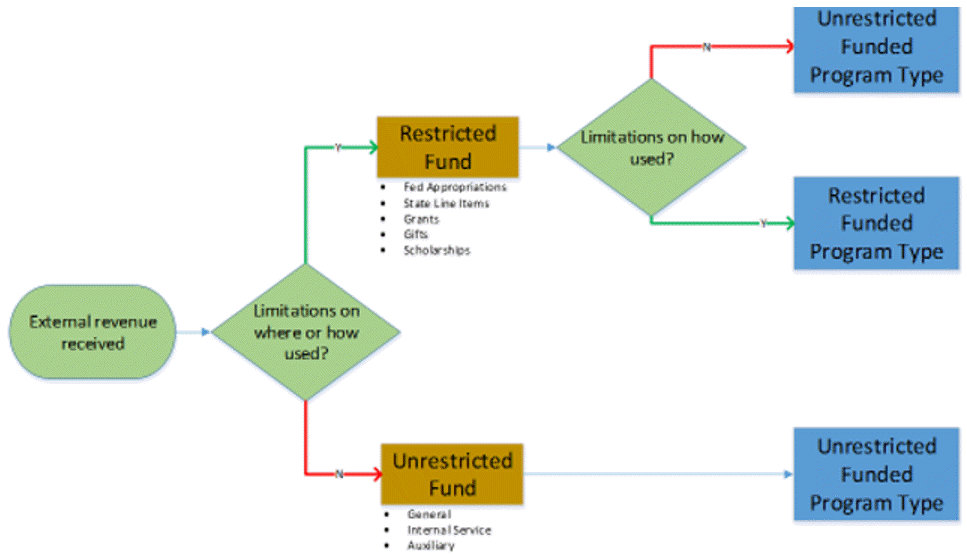

Fund-Funded Program Type Determination Diagram

Restricted/Unrestricted/Designated Defined

Use of Fund, Funded Program types, and Dept. Acct Classifications will be strictly governed to ensure accurate and meaningful reporting.

RESTRICTED

Revenue that is received by the University with limitations on where (by what dept.) and/or how (for what expenses) the funds can be used

- Fund: Gifts – 53010000

- Funded Program Type: Restricted Gifts – Identifies gift accounts which have restrictions from the donor on the use of the funds (except to specify what unit is to receive the gift). The restriction type is determined by the Purpose Code that is assigned to each gift by UDO

- Professorships

- Other Faculty Support

- Facilities

- Programs

FUNDED PROGRAM TYPE EXAMPLES FOR GIFT FUNDS

| Revenue | Fund Type | Funded Program Type |

|---|---|---|

| Gift to Convocations for use at Director’s discretion | Restricted | Unrestricted to Dept |

| Gift to Convocations for supporting piano performance | Restricted | Restricted – Programs |

| Gift to Convocations for use at Director’s discretion but dedicated by Director to supporting piano performance | Restricted | Unrestricted to Dept |

| Gift to the Dean of Liberal Arts for use at his discretion | Restricted | Unrestricted to Dept |

| Gift to the Dean of Liberal Arts for use at his discretion but used to fund faculty research grants | Restricted | Unrestricted to Dept |

| Gift to the Dean of Liberal Arts for use at his discretion but used to fund Startup | Restricted | Startup |

| Gift to the Dean of Liberal Arts for use at his discretion but committed to a building renovation | Restricted | Unrestricted to Dept |

UNRESTRICTED

Revenue that is received by the University without limitations on where (by what dept.) and/or how (for what expenses) the funds can be used. Certain types of activities that can be supported by unrestricted funds are institutionally significant and need to be categorized and identified for reporting and management

- Fund: Gifts – 53010000

- Funded Program Type: Unrestricted to Department Gifts – Identifies gift accounts that have no restrictions on their use, beyond specification of which department is to receive the funds.

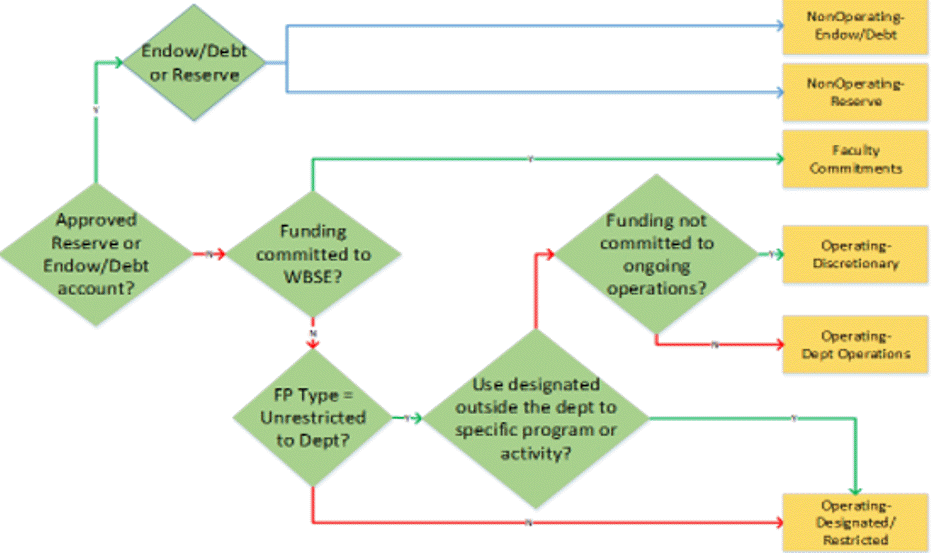

DESIGNATED

Funding transferred from one department to another department with a limitation that the funds be used for a specific purpose, project, or activity within the department.

- Department Account Classification and Institutional Group Descriptions: Operating-Allocated, Operating-Reserves.

- The below table outlines Non-Operating vs. Operating classifications.

| Non-Operating | Operating | |||

|---|---|---|---|---|

| Institutional Grouping | Non-Operating | Operating | Faculty Allocation | Grants |

| Dept Account Classification | Capital | Operating | Faculty Allocation | Grants |

| Reserves – Capital | Operating – Allocated | |||

| Reserves – Equipment | ||||

| Reserves – R&R | ||||

| Reserves – General | ||||

| Reserves – Institutional | ||||

| Debt | ||||

OPERATING VS. NON-OPERATING DETERMINATION DIAGRAM

ENDOWED/NON-ENDOWED GIFTS

Scholarship Endowments

- Endowments for a department that have the same set of restrictions will maintain separate funds at PRF but will distribute revenue to a single shared support account for each set of restrictions.

- Example: Three named endowments supporting instruction will share an account

- Example: Two named endowments supporting piano performances will share an account

- PRF will be accountable to report distributions from all endowments.

- Purdue will be accountable to report expenses related to the purpose defined in the endowment agreement, but not to report what source funded any specific expense(s).

- Example: A department must be able to report what instructional activities it supported, but not what specific instructional activities were charged to general funds, gifts, etc.

Non-Endowed Gifts

- Units will have one unrestricted scholarship account and one unrestricted gift account.

- The creation of any new accounts to receive non-endowed gifts (for either scholarships or gifts) will have to be approved by the VP for Development and Comptroller.

- Non-endowed gifts with restrictions should not be solicited by Directors of Development.

- Unsolicited, non-endowed gifts received with restrictions will be reviewed on a case-by-case basis for appropriate action/management.

New non-endowed gifts of less than $25K per year

- Will not be solicited for restrictions, which necessitate the creation of new accounts.

- Restrictions must be limited to established purposes already tracked (i.e. assigned an account) by the department.

- Or for new purposes for which the department expects to cumulatively receive >$25K in one year.

New non-endowed gifts between $25K and $100K per year

- Should be deposited into an existing gift account if one for the specified purpose already exists.

- Can only have restrictions for purposes not already tracked by the department if the funds can be spent within 24 months.

- Example: If a department does not already have a graduate education gift account, restrictions on a $40K gift stipulating that it be used to support graduate education should only be accepted if the department expects to spend $40K on graduate education over the next 24 months.

- If a department doesn’t expect to be able to use the funds in that period, the gift is too restrictive

New non-endowed gifts greater than $100K

- Can be tracked separately if funds can be spent within 36 months.

SCHOLARSHIPS

SCHOLARSHIP ENDOWMENTS

In December, departments receive projection of maximum distribution for each endowment in the subsequent fiscal year.

- Max distribution policy set by CFO; projection prepared centrally for all endowments

In spring, departments select scholarships recipients and match them to the endowments for which they are the designated selector.

- Awards are entered into the DFA scholarship database by endowment

- Endowments are mapped to unique detail codes in Banner for each scholarship

In fall, awards are applied and expenses posted.

- Each business area has one scholarship IO for all endowed scholarships

- All endowed scholarship detail codes are mapped to the single, shared scholarship IO

- All endowed scholarship expenses post to the single IO

In October, a report is provided to PRF of the awards made from each endowment.

- Distributions are set to equal each endowment

- Distributions post to the single scholarship IO – account balances to $0

In spring, award posting and distribution process is repeated.

NON-ENDOWED SCHOLARSHIPS

Separate accounts for new non-endowed gift and scholarship revenues will not be created, except by approval of the VP for Development and Controller.

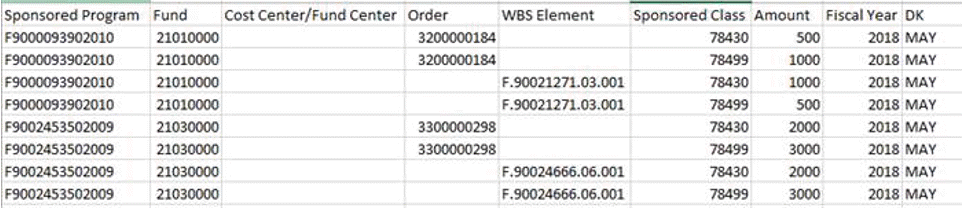

Information from Form 32(s) is entered on the Cost Share Tab in GMGRANT

Fields used for budget entry (ties to how WBSE/SP are established):

- Sponsored Program

- Fund

- Fields use for JV (source account funding the cost share):

- Cost Center/Fund Center (I have recommended this be removed as it is unlikely this will be used)

- Order

- WBSE

Fields used for both:

- Sponsored Class

- Amount

- Fiscal Year

- DK

Once the information is entered on the tab, the budget is created in GM and automatically pushed to FM. The program should then reverse the FM budget

JV(s) prepared to move cash from funding source to grant.

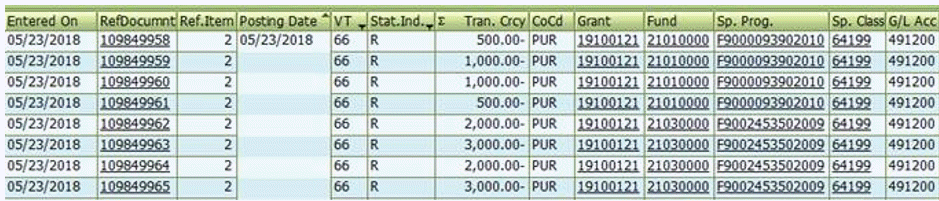

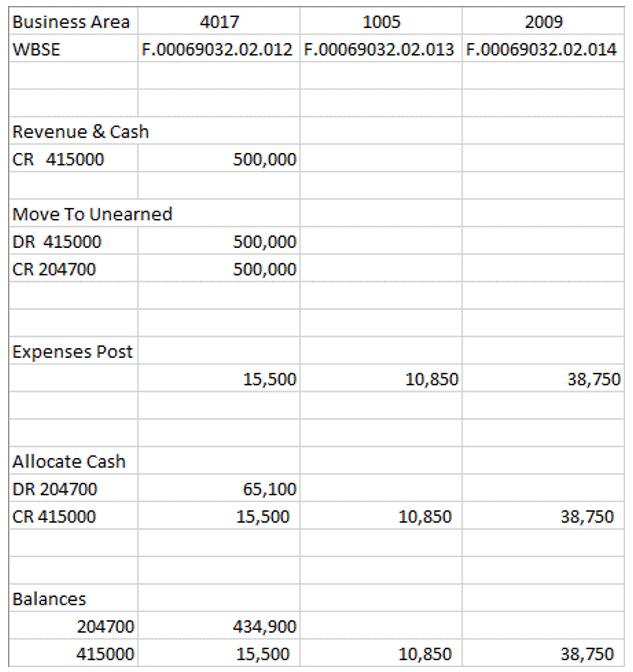

SPONSORED PROGRAMS – GRANT CASH

The overarching principle allocates revenue based upon expenditures and will provide a consistent process for all grants/billing rules (excluding Voluntary Support).

The program will be run nightly to:

- Reads line items per grant

- Reads total expenses per WBS element (GL Account = 5xxxxx)

- Reads total revenue (GL Account 415000)

- Reads total unearned revenue (Account 204700)

- Reads total accounts receivable (102510) debit entries and credit entries. (This amount will stand in for cash)

- NOTE: Does not include reversal documents or documents that have been reversed.

Creates journal entries to move amounts between revenue and unallocated revenue

- Revenue of grant is equal to the lower of either cash received by the grant or the total grant expenses

- Any booked cash in excess of total expenses should be moved to unallocated revenue

- Any booked revenue in excess of either total cash or total expenses should be moved to unallocated revenue

- Revenue of each WBS Elements within grant based upon the proportion of total expenses, up to the total cash received

Example:

VOLUNTARY SUPPORT

New Voluntary Support administration processes was effective July 1, 2024. Questions about the new process can be sent to volsupportquestions@purdue.edu. Process resources can be found below.

Process Training Materials and Resources:

Voluntary Support Process Training PPT

SuccessFactors: New Voluntary Support Process Training (FY25)(LMS 96003)

Quick Reference Guide: Invoices for Voluntary Support Payments

Voluntary Support Invoice Template

Classification, Administration and Reporting of Nongovernmental Support (Policy Reference Including Definitions)

Reporting and Depositing a Voluntary Support Check:

Initiate the Form 44 Approval Flow, through the Qualtrics tool link below, to identify the appropriate approval routing and deposit path for the check. For those needing sponsor code information, there is a link within the DocuSign that provides sponsor codes. Survey responses will populate a DocuSign with the routing required to obtain the necessary approvals.

QRG for Form 44/Voluntary Support Processing

Start the Form 44 Approval Flow (Qualtrics Tool)

Voluntary Support Process Change Questions and Answers

What is the university definition of Voluntary Support?

Voluntary support includes awards and donations from individuals, corporations, partnerships, foundations, associations, and other nongovernmental entities who provide this support without receiving or expecting equal value in return from the University. These awards and donations are further characterized by only minimal reporting requirements to the donor in the form of a general statement of how funds were used.

Additional information, including the definition of contract support can be found in: Classification, Administration, and Reporting of Nongovernmental Support (II.B.6)

Can multiple checks and/or accounts be combined into one account?

Yes, this should be fine as long as the identifying content is the same (PI). We should expect a WBSE associated with individual faculty members where identified; utilizing an existing WBSE is acceptable where identifying content is the same.

Many of our PI’s have multiple VS accounts so we would want to add additional info to the WBSE naming convention you described. I assume that is ok as long as it starts with the info you require, correct?

Yes, that’s fine, as long as it starts with the convention identified.

In the past, we have been able to make the choice to combine voluntary support gifts to one PI from different sponsors if we wish to. Sometimes we wish to keep them separate — sometimes we wish to combine them. I assume both of these options are still fine depending on our business need.

Yes, would not expect that to change. Discretion for the allocation is up to the department to best determine.

Is the DocuSign form one you will be able to track or is it like the Power Forms that are not trackable?

As initiator, you will be able to track the docusign signers as the workflow progresses.

What if you have a check that needs to be split into more then one account. Will you be able to add more then one account to the form 44?

No. Separate documents are expected, as the allocation is tied to the individual researcher.

I’m assuming we obtain the docusign approval before doing the actual FV50 deposit?

“Yes, all approvals are expected prior to the deposit of the check, which represents acceptance of the voluntary support.

From an operational perspective, a document may be parked until all approvals are received; then attach the Docusign to the document, and save as complete.”

Will there be a report of all 300* Grants to begin creating the WBSE’s following the new process? Or will these be allowed to remain as is?

Funds already received and deposited to 02 nodes may continue to be spent. At a to-be-determined date, we expect to address the process in the future. There will be a report out so that departments can create the WBSE’s needed and/or identify to which WBSE the funds will be transferred if already created. Also, will need to be mindful of overdrafts and have those cleared up. More information will be coming early in the next fiscal year.

Are there restrictions for usage of voluntary support?

There are no restrictions for use by the identified faculty researcher.

What should be utilized in the deposit header?

The sponsor number and sponsored name should be identified in the deposit header. (Example: VS_407517_Syngenta)

The check I received is not in support of an individual researcher; is there a change to the process?

If the check is not provided for the use of an individual researcher, it would be considered a gift rather than voluntary support. The qualtrics tool will provide routing to the version of the form 44 designated for gift processing. There are no other associated process changes for this type of gift, it will still be provided to Purdue For Life for deposit.