Finance Structure and Master Data

The following master data elements and financial structure are clearly defined. It is important for finance staff to understand what each element represents, how elements are classified and are used within the structure. Three decision trees, Funded Program Type, Department Account Classification and Faculty Allocation Nodes help the requestor or creator of the internal order/work breakdown structure identify the best fit. The Introduction to Master Data training in Success Factors LMS (Learning Management System) outlines the below information and provides a resource documentation that lists funded program types, defines department account classification and institutional grouping, lists type rollup by fund and funded type program and when to create an internal order vs. WBSE for faculty allocations.

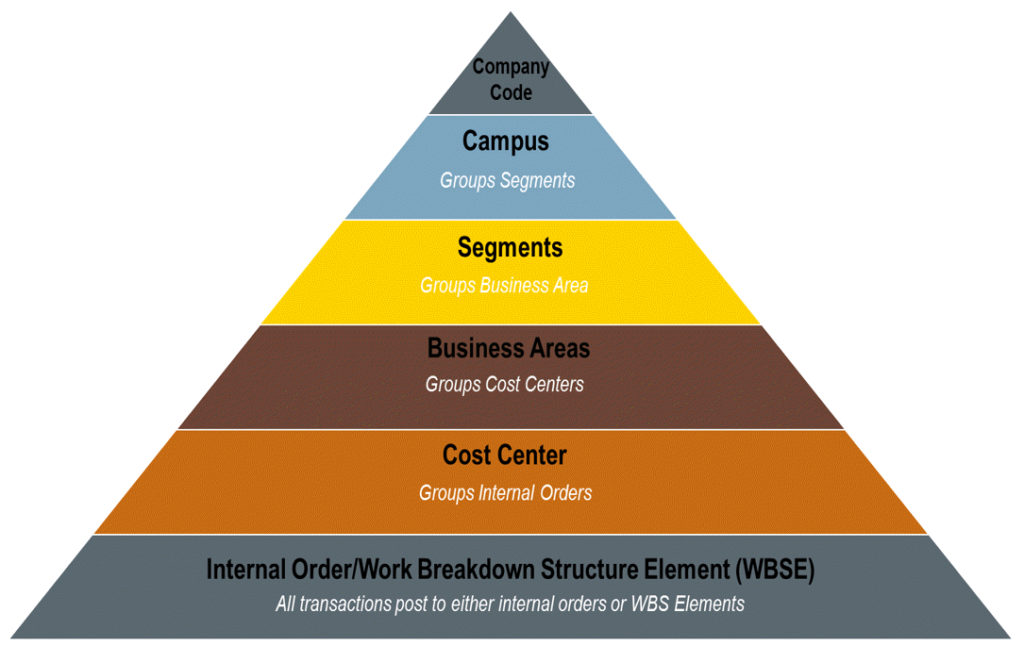

FINANCE STRUCTURE

FINANCIAL/ORGANIZATIONAL (FINANCIAL REPORTING) STRUCTURE

STRUCTURE TERMS AND DEFINITIONS

INTERNAL ORDER & WORK BREAKDOWN STRUCTURE ELEMENT

- IOs and WBSEs are the lowest level of the accounting structure.

- WBSEs are the equivalent of an IO and are used for faculty allocation accounts.

- All other organizational data elements are derived from the IO/WBSE:

- Cost Center

- Business Area

- Segment

- Campus

- Company Code

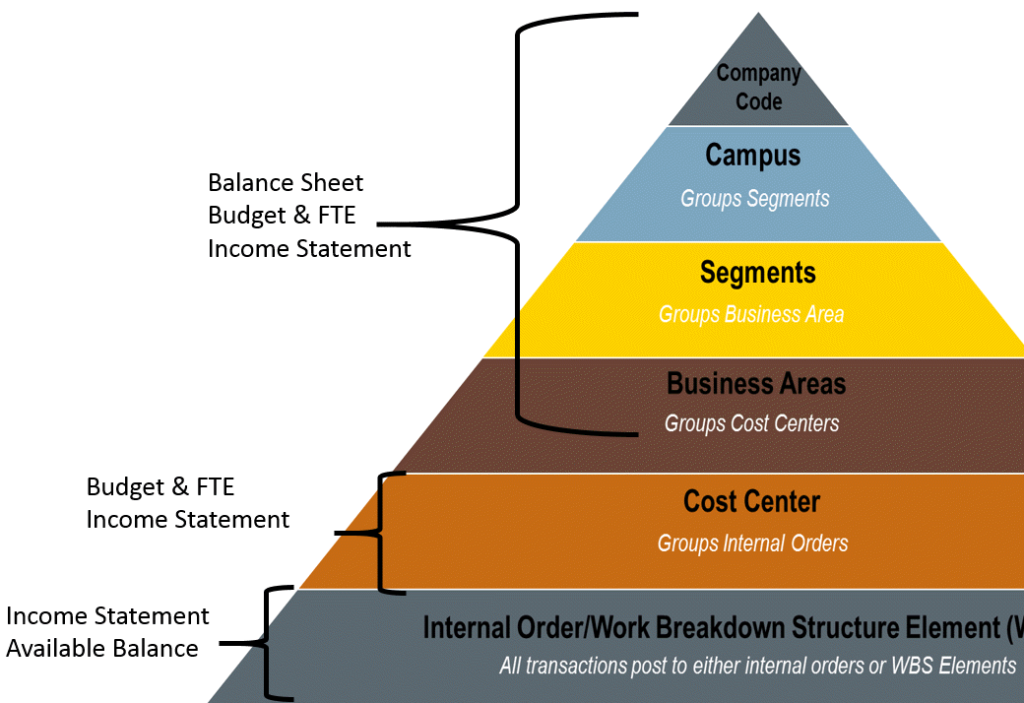

- Income statements (revenue, expenses, transfers) are available for all IOs/WBSEs.

- Available balance is calculated at the IO/WBSE level.

- IOs/WBSEs are created primarily by business office staff.

- In FM, IOs/WBSEs are matched with an identical Funded Program.

COST CENTER

- Cost Centers represent organizational units to which IOs/WBSEs AND positions are assigned.

- There are very limited exceptions to this requirement which include Central Office cost centers and Recharge/Digital Ed cost centers.

- Every Cost Center in the Finance structure has an equivalent Department (i.e. Org Unit) in the HR structure.

- Creation of a new Cost Center requires the approval of both HR and the Comptroller’s Office to verify need.

- Income Statements (revenue, expenses, transfers) are available for all Cost Centers.

- FTE and Headcount is available for all Cost Centers.

- Capital assets are also tracked by responsible Cost Center.

- Cost Centers in FI/CO will be matched with an identical Funds Center in FM.

- Cost Centers can ‘roll-up’ to another Cost Center and are arranged in a three-level hierarchy: Financial Unit, Financial Sub-Unit, and Program.

- Financial Units are required to have annual budget plans.

- Annual budgets are optional for Financial Sub-Units and other Cost Centers.

- Lower level Cost Centers should still represent units which own positions, have a leader, and have accountability for determining how funds are used.

- Cost Center Category and alternate hierarchies will be used for some reporting needs

BUSINESS AREA

- A Business Area is primarily a grouping of Cost Centers.

- Income Statements (revenue, expenses, transfers) are available for all Business Areas.

- Business Areas represent:

- Colleges

- Athletics Departments

- Units led by individuals who directly report to a Segment Executive and have annual expenditures greater than $7.5M

- Units which have a reporting requirement that necessitates an SAP-generated balance sheet.

- Business Area is the lowest level

- Some components are tracked at lower levels.

- Capital Assets at the Cost Center level.

- Some are only tracked by Business Area.

- Cash, Inventory

- These components are not attributed to a Financial Unit or Cost Center, but can be reconciled to them

- Some components are tracked at lower levels.

SEGMENT

- Segments are simply groupings of Business Areas.

- Segments represent the grouping of Business Areas for which each Executive is responsible.

- No financial information is available for segments that isn’t already available for all Business Areas.

CAMPUS

- Campus reporting in the future is accomplished by grouping segments

- For example: Purdue West Lafayette, Purdue Northwest and Purdue Fort Wayne.

COMPANY CODE

- Separates distinct legal entities which have entries in SAP

- For Example: Purdue Applied Research Institute, Purdue Global, and Purdue University.

FINANCIAL INFORMATION VS. FINANCIAL STRUCTURE DIAGRAM

MASTER DATA

WHY IS MASTER DATA IMPORTANT?

Master Data is the basis of all external and internal University financial reporting

Master data derives the following on postings:

- Fund

- Funds Center

- Functional Area

- Business Area

FINANCIAL ACCOUNTING (FI) VS FUNDS MANAGEMENT (FM) VS GRANTS MANAGEMENT (GM)

SAP Ledgers – Differences Between

Financial Accounting (FI)

- Reporting is based on GAAP

- Provides Balance Sheets and Income Statements

Funds Management (FM)

- Reporting is based on budgetary management

- Calculates available balance

- Provides Income Statements

Grants Management (GM)

- Facilitates both financial accounting and budgetary management by grant

WHAT IS MASTER DATA?

FUNDS

- Represent a particular funding source and restriction

- The fund derives when the Work Breakdown Structure Element (WBSE) or Internal Order (IO) are entered based on the funded program type

- List of Funds

FUNDED PROGRAM TYPE, ORDER TYPE, PROJECT TYPE

- Order Type (IO) and Project Type (WBSE) = Funded Program Type (FP)

- Funded Program Types reflect restrictions and/or categorizations defined by Purdue for reporting

- These Types derive:

- The numbering range for internal orders (IO)

- The Fund that transactions are posted to

- Many funded program types may point to the same fund

- Exceptions are handled by manual entry into a table by the master data team

- Funded Program Types are grouped into Funded Program Type Rollups for reporting

- Example: Unrestricted Rollup includes – Unrestricted General, Unrestricted Extension, Unrestricted Research, and Unrestricted Gifts

- Selecting Order Type, Project Type, Funded Program Type

- Consider: Fund, Attribute, Activity

- Finance Structure and Master Data

- Funded Program Type Decision Tree

INTERNAL ORDERS (IO)

- Used for detailed tracking within Cost Centers

- Individual Programs

- E.g. Study Abroad, Digital Education programs, Conferences

- Individual restricted gifts/scholarship accounts

- Are assigned to cost centers at the Financial Unit, Sub-Financial Unit, and Program levels

- Should not be used to track Faculty Allocations

- Should only be set up for activities that will have a high dollar value of activity and business decisions will be made based on review of account activity

- Internal Orders are reviewed prior to being released

- Quick Reference Guide

WORK BREAKDOWN STRUCTURE ELEMENT (WBSE) FOR FACULTY ALLOCATIONS

- Utilizes a Work Breakdown Structure Element (WBSE) and the faculty members Person ID from their HR record

- Structure Allows:

- Faculty to review all of their accounts in one view using a common numbering sequence

- Departments to identify and segregate resources allocated to faculty for their activities

- Account to be assigned to both the responsible department and the responsible faculty member

- Faculty members can have accounts in multiple departments and business areas under the same structure

- IMPORTANT things to remember when establishing a Faculty Allocation WBSE

- Use the Person ID not the PERNR

- Use ECP to look up the Person ID

- Work Breakdown Structure Element

FACULTY ALLOCATION NODES

- Federal Appropriations and Matches (Node 1) – Ag, Vet, HHS only

- This node will only be used by units with federal appropriations and matching funds

- WBSE’s will be established to track what portion of a faculty member’s salary is charged to the department’s allocation of federal appropriations, state line items, or general funds

- WBSEs in this node will be child accounts

- Grant (Node 2)

- This node will hold grant accounts for the faculty member when they are listed as the Co-PI of the Sponsored Program

- Only SPS can create accounts in this node

- Faculty Discretionary Use (Nodes 3 and 4)

- Accounts do not have restrictions on types of expenses or on projects/programs benefitted by expenditures

- Examples: Research Discretionary, Faculty Scholar Allocations, Grant or Digital Education Residuals, Faculty Awards

- Allocations that have expiration dates but no other restrictions should be assigned the Discretionary node

- Accounts in node 3 do not have a parent, but node 4 require a parent

- Accounts do not have restrictions on types of expenses or on projects/programs benefitted by expenditures

- Faculty Startup (Node 5)

- Used for Start Up Allocations provided to a faculty member

- Multiple WBSE may be created based on the departmental restrictions and reporting requirements for Start Ups

- Start Up Allocations must have a Parent Account

- Institutional Attribute for both the WBS and the Parent must be SU (Start Up)

- Endowment Field must contain the fiscal year of the first year of the Provost Start Up and the word START

- Example: Provost funding started August 2019, then enter 20START

- Restricted Use (Nodes 6 and 7)

- Contain Internal grants and other allocations that support a faculty member’s activities with specific restrictions for the use of the funds

- Examples: Research Seed Grants, Research Lab Upgrade, IMPACT Allocations, Allocation given for specific travel, Equipment Allocation, Grad Allocations

- See Institutional Attribute section for more information on Internal Grants.

- Funded Programs in node 6 do not have parent accounts and node 7 funded programs must have parent accounts

- Contain Internal grants and other allocations that support a faculty member’s activities with specific restrictions for the use of the funds

- Decision Tree

PARENT/CHILD RELATIONSHIP

- A parent is a funded program that combines or “rolls up” the activity of child funded programs

- This relationship facilitates tracking of specific revenues and/or expenses with a program or activity

- The parent and the child MUST have the same

- Fund

- Funded Program Type

- Business Area

- Cost Center

- Institutional Attribute

- State Line Attribute

- A child account can be an IO or a WBSE, BUT a parent account can ONLY be an IO

DEPARTMENTAL ACCOUNT CLASSIFICATION (DAC) AND INSTITUTIONAL GROUPING (IG)

- Institutional Grouping (IG)

- Classification for reporting that categorizes transactions and balances into Operating, Non-Operating, Faculty Allocations, and Grants

- Derived from information entered into the Department Account Classification (DAC) field

- Departmental Account Classification (DAC)

- Lower level of classification that rolls up to Institutional Grouping (IG)

- The DAC is entered on the Internal Order (IO) or Work Breakdown Structure Element (WBSE)

- Decision Tree can be used to determine appropriate DAC.

INSTITUTIONAL ATTRIBUTE

- A listing of the institutional attributes can be found on the Finance Structure and Master Data Resource.

- Things to know about Institutional Attributes

- SU (Start Up) should only be used on WBSE in node 5

- If it is an IO, the IO should be a parent to WBSE with the SU attribute

- If SU is on the WBSE, the endowment field 1 should have the two-digit fiscal year that the Provost start up package was given and the word START.

- Example: The faculty member received his package in August of 2019 so you would enter 20START

- If IG (Internal Grant) is listed, the following fields need to be completed:

- Endowment 1 Internal Grant Award

- Endowment 2 Business Area providing funding for the award

- Endowment 3 Financial Unit Funded Program providing funding for the award

- Endowment 4 BA Acronym providing funding for award

- SU (Start Up) should only be used on WBSE in node 5

- See Finance Topics – Internal Grant for more information

OTHER ATTRIBUTES

- State Line Attribute – Some state line items and federal line items have their own funds but in other cases they have the same fund so the state line attribute needs to be selected to assist with reporting

- Valid to Date (IO) or Closing Date (WBSE) – This must always have a value. If there is not a known expiration date, then 12/31/9999 should be entered. If the account is a Start Up or Internal Grant, then the known expiration date should be entered.

- Long Text – This can be used for additional information. This is also where the IO request template should be saved.

- Parent Funded Program – This will be completed with an IO number if the IO or WBSE is a child account.

PUBLIC/NON-PUBLIC/MIXED

- Restrictions exist on what type of investments and purchases can be made with public money; this designation allows us to understand the balance of these types of funds

- This categorization designates whether an account includes public funding. Public funding is defined as Tuition and Fees, Federal/State Appropriations, and Federal Grants & Contracts revenue. Public funding also includes any accounts that receive Recurring Allocation since it is primarily made up of Tuition and Fees and State Operating Appropriations.

- Non-Public Funds include Gift revenue, Sales and Services revenue, Investment Income, and Other Operating Income

- Mixed Funds contain both public and non-public funding

FUNCTIONAL AREA

- Defined by NACUBO and categorized by expenditure function

- Assigned to an individual IO/WBSE

- Used for financial reporting, IPEDS data, and external report of research spending

- There is a correlation between Funded Program Type and appropriate Functional Area

- Instruction & Departmental Research (1000 – 1050)

- Organized Research (1200 – 1400)

- Extension and Public Service (1500)

- Academic Support (1600, 1100)

- Student Services (1700)

- General Administrative & Institutional Support (2000 – 3000)

- Scholarships & Fellowships (4xxx)

- Auxiliaries (5xxx)

- Plant (1800)

- Functional Area Grid