Accounting And Financial Management Governance – Transfers (current)

WHAT IS A TRANSFER?

A transfer is the movement of funds between accounting elements within the University. The following sections will provide general guidelines for University transfers and specific information for FY 2020 updates.

Use of transfers should be done as a last resort. Many transactions can be posted with a split on the original purchase, posted as a reimbursement of supplies, service or other expense, or recharged for services provided. Defining the correct elements and transaction process for moving funds or “cash” between accounts requires more detailed information as this movement creates mismatches between allocations of revenue or expense and has an effect financial statements. The new Segment Transfer CI’s implemented for FY 2020 are designed to help create transparency about how cash is being moved between University entities. Business Offices should only be using those commitment items included in the All Business Areas section of the General Ledger Transfer Review.

A set of audit reports is being developed and will be reviewed regularly by Accounting Services to look for a violation of the guidelines and processes Accounting Services will be emailing the preparer, DFA and Senior Director for any issues found.

The resources below show the thought processes that can be used to decide what type of document should be used, and what commitment items to use.

CURRENT FY TRANSFERS

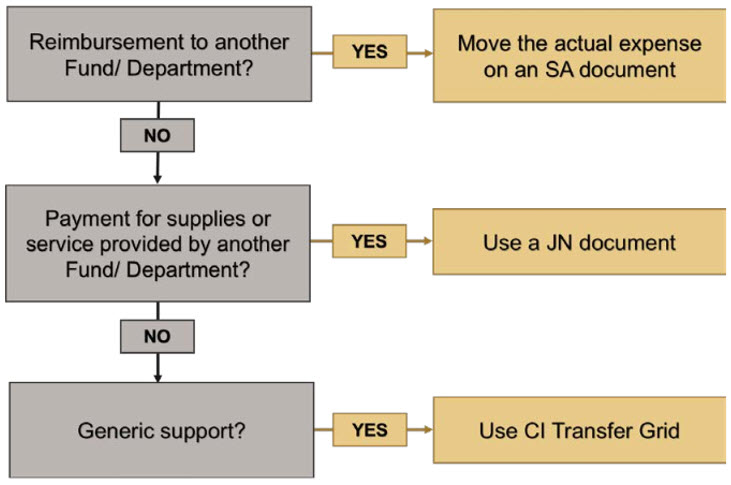

IS A TRANSFER REQUIRED?

The transfer decision tree below can be used to help determine how to properly report revenues and expenses so financial statements are kept accurate and transparent.

See below for a visual decision tree.

Step 1: Was the revenue or expense charged to an incorrect account?

If yes, then complete a JV with a SA document type using the same Commitment Items (CI) as the original transaction. This would be considered a Correcting Document. Keep in mind that this type of transaction will be scrutinized in the event of an audit. The transaction must be allowable and allocable.

- Example 1: Professor X orders supplies on a grant account; after reviewing financial reports, the supplies should have been charged to a discretionary account.

- Example 2: In a review of his account, Professor Y notices that Professor Z’s travel posted to his grant in error. A correcting document needs to be done to move these expenses to the correct funding source.

- Example 3: Business Office Student Organizations (BOSO)- If reimbursement of expense is needed, then a journal voucher (document type SA) debiting IO 7200000100 should be processed. If the expense is for food obtained from external vendors, then the CI should be 546010 – Student Function-External. If the expense is for any other expense associated with student orgs, then the CI should be 546090 – Student Function-Program Support.

If no, then go to the next question.

Step 2: Is the money being used to pay for a purchase of supplies, receipt of a service, or other expense provided by another account/financial unit within the University?

If yes, then use a JN document type (Intramural Invoice Voucher) to bill the purchasing account for the goods or services purchased using revenue and expense Commitment Items. The JN document type is only used for revenue and expense transactions. A JN document type is never used with a transfer Commitment Items (49XXXX or 59XXXX). Generally, JN documents are only used with an approved rate.

- Example 1: Conference Account – Associate Dean needs to pay for a registration through Purdue Conferences from their faculty allocation account.

- Example 2: Recharge Subsidy

- Regardless of the types of Funds being used to subsidize a recharge, the recharge subsidy Commitment Items are required to be used. Continue to use Recharge Subsidy Income (433080) and Recharge Subsidy Expenses (S&W- 505070, RS Fringes- 512900, and RS S&E-523110) Commitment Items for these subsidies. Recharge Subsidies are required to balance.

If no, then go to the next question.

Step 3: If neither of the above scenarios fit, you may need to process a transfer document. In order to mitigate the negative impact transfers have on University Financial Statements, transfers need to be closely scrutinized. Review the Guidelines shown below in this document for full review questions. However, if the money is being used to provide generic support with no specific guidelines on how it is to be spent, then process a JV with a SA document and use the new CI Transfer Grid (See Appendix B) for appropriate CI’s.

- Example 1: The Provost is providing funds across the University for Faculty Start Up.

- Use CI 491035 – Transfers-To/From PROV/VCAA Area

- Example 2: College A is supporting a department faculty members Post Doc.

- Use CI 491065 – Transfers-Between Financial Units (w/in same BA)

- Example 3: Business Office Student Organizations support

- Use CI 491055 – Transfers-Between Business Areas

DECISION TREE

TRANSFER GRID

TRANSFER GUIDELINES

The purpose of these guidelines is to change the practice of defaulting to transfers for all situations. The original purpose of the guidance to reduce transfers was intended to reduce the negative impacts on financial statements and distortion of revenue and expense trends and reporting. Therefore, before processing a transfer, users should focus on the bigger picture to improve financial transparency and decrease transferring and tracking small dollar amounts. Users should focus on recording expenses where it belongs at the time the purchase or service, which in turn will reduce transfers overall.

The following types of transfers are either not allowed, or need close review.

- Transfers between Institutional Groups – this has an effect on the original funding source of money

- Approved Exceptions

- Operating to Faculty Allocation

- Central Office Use (Cost Share, R&R, etc.)

- Student Organization Support

- Approved Exceptions

- Transfers between Funded Program Type – this has an effect on the original funding source of money

- Approved Exceptions

- Ag, Vet & HHS can transfer between the three different types of General Funds

- Transferring residual funding

- Student Organization Support

- Approved Exceptions

- Transfers between other Funded Program attributes such as Functional Area, Public/Non-Public, Restricted/Non-Restricted, etc.

- Transfers for less than $1,000 per line item will not be permitted

- Approved Exceptions

- Close a master data element.

- Student Support

- Student Awards

- Student Research Allocations

- Student/Faculty Mentoring programs

- Student participation in national organizations or events

- Student Travel Grants

- Student Organization Support

- Faculty Allocations

- Research Incentive Funds Allocations

- Faculty Service Learning Grants

- Professional Development Funds

- Faculty Mentorship allocations

- Approved Exceptions

Additional attention should be paid to decisions around deciding what should be included in any document, focus on being able to accurately describe what the purpose of the document is (in document header), rather than focusing on the number of documents or line items.

-

- Use separate documents to help with improving the approval flow speed. For example, separate out by Business Area.

- Separate transfers for like topics, i.e. Instructional Equipment or Start-Up.

- You are required to have backup documentation and it should be attached so that the information will be available in WebNow. Don’t use the long text except to put a summary in SAP.

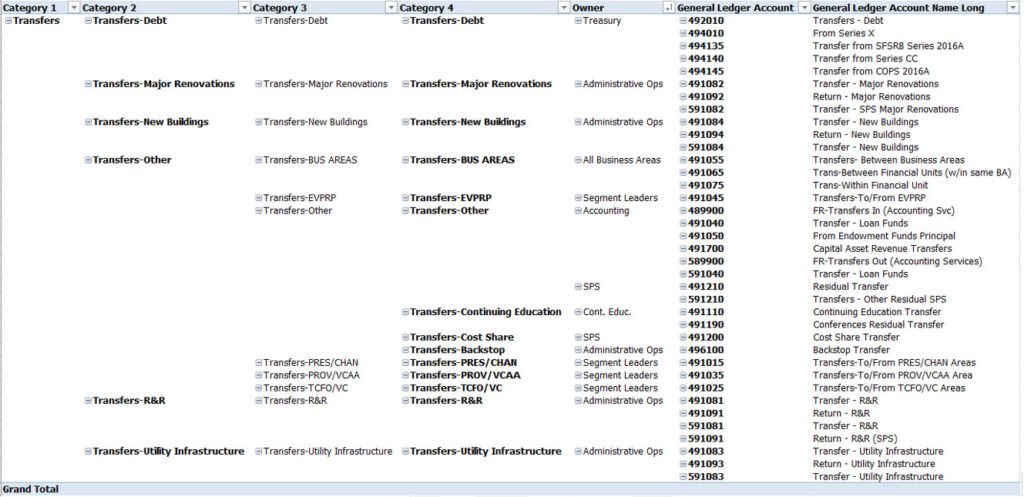

GENERAL LEDGER ACCOUNTS

NOTE: Category titles may change in Fiscal Year 2020

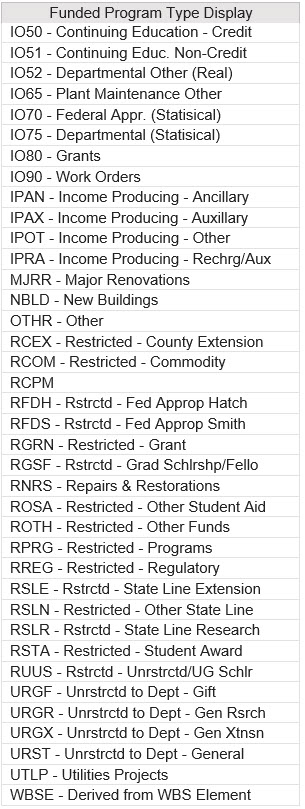

FUNDED PROGRAM TYPES

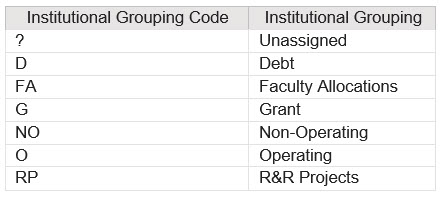

INSTITUTIONAL GROUPS

HOW TO ENTER A TRANSFER DOCUMENT

- Create Journal Voucher

- Basic Data

- Use document type SA

- Header Text should be used to describe what the document as a whole is accomplishing. This can be found in several transaction reports.

- Use the specific Commitment Items from the new CI Transfer Grid (See Appendix B)Sender account should be entered as a debit (reflected as a positive amount)

- Receiving account should be entered as a credit (reflected as a negative amount)

- JV upload tool Debit = 40 & Credit = 50

- Enter the amount without signs

- Use the Line item text to describe what each line of the document is doing. This will also show in transaction reports after processing.

- You must enter either an Order or a WBS element

- “No hops” are allowed, i.e. send the funds directly to the entity who should receive the funds, don’t temporarily send the funds to one entity which will move it to the final recipient

- Support documentation explaining the purpose of the document should be attached. See the FB03 – Attachments and Workflow for instructions.

- Without proper backup documentation, the fiscal approver will send back your document requesting more documentation

- Use the Reference, Line Item Text, Long Text, and Header Text fields to help explain the transaction.

- Debits and Credits at a Commitment Item level should balance

- Validate that the document balances to zero by CI

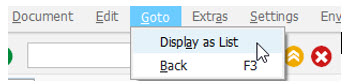

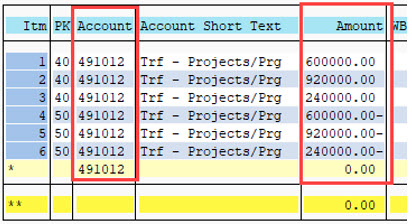

- T-code FV50 to display document click Go to > Display as List

- Click on the “Amount” column and click the Total icon

- Click on the “Account” (GL) column and click the Subtotal icon

FISCAL YEAR 2020 UPDATES

Updates for FY 2020 are shown below and in the 2020 Transfer Process Updates training materials.

- Subdivided the Category 3 “Transfer-Other”

- Improves visibility in reporting

- Displays monies Sent/(Received) from a Segment

- President/Chancellor

- Treasurer/Vice Chancellor

- Provost/Vice Chancellor for Academic Affairs

- EVPRP (Specific to BA 4007)

- Displays monies Sent/(Received) between all other Business Areas

- Between BA (All other BA not specified in the unique segment)

- Between Fin Unit (Fin Units within the same BA)

- Within FinUnit

- If transfers are completed between Segments, i.e. the President transfers funds to the Provost, then the “Sender” Commitment Item is used.

- Use the General Ledger Transfer Review document for a full listing of Transfer CI’s.

FY 2018-2019 Transfers

Transfers FAQs (Current)