COVID-19 Impact on Gas Tax Projects

By LTAP's Research Manager Pat Conner

The Motor Vehicle Highway Account (MVH), Highway Road and Street Account (LRS), and the Local Road and Bridge Matching Grant Fund, more commonly known as Community Crossings Matching Grant Fund (CCMGF), are all funded by the purchase of gasoline and/or diesel fuel. How these funds are impacted all vary due to other revenue sources that also contribute to these accounts and grants. These funds and grants are three of the main sources of dedicated transportation funding for our local highway and street departments. The MVH and LRS also impact the funding for the Indiana Department of Transportation (INDOT).

The MVH is composed of the following revenue sources: International Registration Plan (IRP), the State Court Fees, The Gas Tax, Special Fuel Tax, and Gasoline Use Tax. Such sources make up approximately 80% of the MVH fund. The total amount of the MVH fund for FY 2019 was around $1.3 billion, with a little over $1 billion from fuel purchases. Assuming the IRP, State Court Fees, and Vehicle Fees stay constant through the COVID-19 Stay-At-Home Executive Order, the loss of revenue from fuel purchases would significantly impact the MVH fund. One would need to factor in both the loss of revenue of special fuels (largely diesel) and gasoline to accurately determine the impact.

The LRS is composed of a portion of the Special Fuel Tax, a portion of the Gasoline Tax, and a portion of the Vehicle Fees collected through the BMV. Fuel purchases account for about 94% of the LRS account. The total LRS for FY 2019 was about $350 million, with approximately $330 million from fuel purchases.

The CCMGF is comprised of the electric car and hybrid vehicle registration fees, the transportation improvement fee, and a portion of the gasoline use tax. The gasoline use tax is about 50% of the total fund. For FY 2019, the CCMGF was about $194 million of which about $96 million came from the purchase of gas.

The question at this point is: how to do we predict the effect of COVID-19 on the monthly distributions to the MVH and LRS accounts? How does this impact project bids and awards, and construction season plans? One way to measure the potential impact is to determine the change in statewide traffic volumes. Obliviously, if traffic volumes decrease, fuel consumption decreases as well, unless they are stockpiling it along with their toilet paper. In the FHWA Traffic Data Computation Method pocket guide, they describe a method for predicting future traffic volumes by the percent increase in gas tax growth if there is not a system already in place. One approach for calculating fuel revenue would be to do what FHWA recommends in reverse: determine the percent change in traffic and apply that to fuel revenue.

“In the absence of modeling programs, states can use the local population growth or gasoline tax growth rate to estimate the AACR of regional traffic conditions.”

FHWA Publication No. FHWA-PL-18-027, Traffic Data Computation Method, Page 38

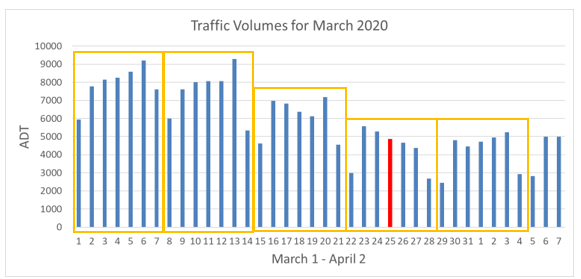

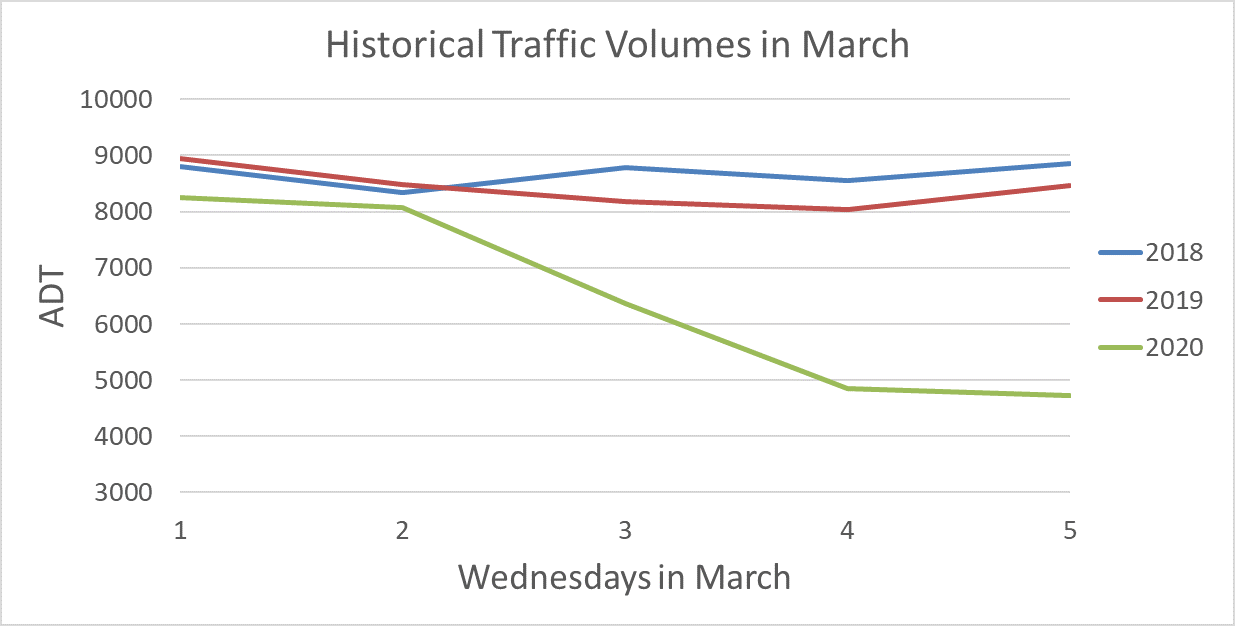

INDOT has numerous sites that continuously count vehicular traffic on its roadways. The data shows there has been about a 45% decrease in light duty vehicles and a 35% decrease in heavy trucks statewide during the week since the Governor’s Stay-At-Home Order. See figure 1 for an example of one of the sites that continuously measures traffic volumes. Figure 2 shows a comparison of Wednesday traffic in March and the beginning of April for 2018-2020. The weekend traffic volume is showing a decrease close to 60%. Assuming the light duty vehicles are all using gasoline and the heavy trucks are using special fuels, we can estimate the decrease in MVH and LRS funds by assuming the decrease in fuel usage is proportional to the decrease in traffic volumes. We estimate the potential drop in the MVH and LRS accounts to be approximately 33% for MVH and 39% for LRS. Note this is a simple estimation due to lack of an accurate prediction model with broad assumptions of the novel scenario created by COVID-19.

Figure 1: SR 231 at RM 196.0 in Tippecanoe County (Example traffic Volume Data)

Figure 2: Example of Traffic monitored on a specific day (SR 231 at RM 196.0)

Taking in account for these broad assumptions, the potential revenue loss can be estimated to be between 30%-50%. For the month of March, traffic was not significantly affected by COVID-19 during the first two weeks of the month. The third week of March we started to see a decline in traffic volumes due to the heightened awareness of COVID-19; then in the fourth week of March we see the 40-45% decrease in traffic due to the Governor’s Executive Order to Stay-At-Home. The reduced traffic volume after the Stay-At-Home Order seems to be constant as the order continues and is extended. The May distribution of the MVH and LRS should see a partial impact due to about 1/3 of March being impacted. This partial impact for May would be estimated to be between 10%-20% of you’re 2019 distribution. Then every month after May you should see a full impact (30%-50%) as long as the Governors Stay-At-Home Order is in effect. These estimates are assuming a proportional relationship between a percentage of ADT drop and percentage of gas tax drop.

Here is an example of how to calculate the range of estimated MVH distributions based on ADT assumption:

May 2020 (Partial Effect)

June through the end of Stay-At-Home Order (Full Effect)

The decrease in MVH funds, LRS, and CCMGF is not only going to cause an impact on planned construction projects it is also causing further impacts on the MVH unrestricted funds. The MVH unrestricted funds is proportionally affected. Historically, the MVH funds were all “unrestricted," which meant they could be used to pay for salaries, winter maintenance, insurance, maintenance in the right-of-way, event cleanup, new equipment, helping cleanup or prepare for a natural disaster, along with any highway/street department construction, reconstruction, or preservation projects. In 2017, when the gas tax was increased which has brought about 30% increase in MVH funds, restrictions were added to how local highway and street departments could use these funds. Written in the Indiana Code was the restriction that 50% of the MVH funds needed to be spent on construction, reconstruction, and preservation projects. Between CCMGF and the gas tax increase there has been a significant increase in funds available for new construction and preservation projects! Depending on how much each highway/street department was using their MVH funds for maintenance and overheard related work items, this has caused some agencies a shortfall in revenue for these budgeted line items since many of these line items are also not allowed to be used in the LRS funds, wheel tax funds, or other common funding sources for highway/street departments. Using the example from May above, if a highway/street department was expecting to be able to budget 50% of $225,000 or $125,00 for salaries for their personnel, now there could be up to $56,250 available, a 50% decrease.

- Digital Newsletters

- Vol 38 No 1.1

- Vol 38 No 1.2

- Vol 38 No 1.3

- Vol 38 No 2.1

- Vol 38 No 2.2

- Vol 39 No 1.1